How to create an annual budget that improves cash flow, reduces surprises, and supports better business decisions.

A small business budget helps you plan income, control costs, manage cash flow, and make better decisions before problems grow. Used well, an annual budget is not just a financial document. It is an early-warning system that shows what is working, what is drifting, and what needs attention.

This article explains what a small business budget is, why budgets often fail, what to include, how to build an annual business budget, how to review it each month, and how to use budget variance as a decision signal. It also shows how budgeting supports strategy, cash flow, leadership, and decision-making under uncertainty.

- A small business budget helps you plan income, costs, cash needs, and future decisions.

- The best budget is not just created once. It is reviewed and adjusted regularly.

- A budget should help you spot early warning signs before cash pressure builds.

- Budget variance shows the gap between what you expected and what actually happened.

- Used well, budgeting becomes a decision tool, not just a finance task.

Why small business budgeting matters

Small business budgeting can sound dull.

I understand that.

A budget does not usually make people leap out of bed with excitement! If it does, you may need more hobbies. Or better coffee…

But in real business, a budget is one of the simplest tools for staying in control.

In my experience, many small business problems do not start with one big disaster. They start with small gaps that are not noticed early enough.

A cost rises quietly.

A customer pays late.

A marketing campaign costs more than expected.

A slow month arrives sooner than planned.

A new hire adds pressure before extra income arrives.

A supplier increases prices.

A few “small” subscriptions keep appearing on the bank statement like tiny financial mosquitoes.

None of these things may look dramatic on their own. But together, they can put pressure on cash, profit, confidence, and decision-making.

That is why a small business budget matters.

It gives you a plan.

More importantly, it gives you something to compare reality against.

And that is where better decisions begin.

What is a small business budget?

A small business budget is a financial plan that estimates your income, expenses, cash needs, and planned spending over a set period, usually monthly, quarterly, or annually.

A budget helps you answer questions such as:

How much income do we expect?

What will our fixed costs be?

What costs will rise when sales rise?

What one-off costs are coming?

How much cash do we need to hold back?

Can we afford to hire, invest, or expand?

What happens if sales are lower than expected?

What should we stop, change, or review?

A good budget is not just a list of numbers.

It is a plan for how the business will use money to support decisions.

A small business budget is a practical plan for expected income, costs, cash needs, and spending decisions over a set period.

In plain English: it helps you see where money should come from, where it is likely to go, and what decisions need attention before problems grow.

Useful background reading:

Xero: How to Create a Small Business Budget

SumUp: Small Business Budget Guide

Federation of Small Businesses: How to Create a Small Business Budget

Why is budgeting important for small businesses?

Budgeting is important for small businesses because it helps owners control spending, prepare for slow months, manage cash flow, plan growth, and make better decisions before financial pressure builds.

Without a budget, many business owners end up managing by bank balance.

That is risky.

The bank balance tells you what is there today.

It does not always tell you what is coming next.

It may not remind you about tax, VAT, wages, loan repayments, seasonal dips, supplier bills, delayed customer payments, or that expensive piece of equipment quietly waiting to ruin your Tuesday.

A budget helps you look ahead.

It supports decisions about:

pricing

hiring

stock

marketing

equipment

growth

cost control

cash reserves

debt repayment

new services

business investment

A budget is not just a plan for money.

It is a plan for decisions.

The value of a budget is not only in creating it. The value is in using it to notice when reality starts moving away from the plan.

Idea Bridge: from budgeting to better decisions

Many budgeting guides focus on the mechanics.

Add income.

List expenses.

Track spending.

Review the numbers.

That is all useful.

But it misses the deeper point.

A budget should help you make better decisions under uncertainty.

You rarely know exactly what the year will bring.

Customers may change behaviour.

Costs may rise.

Sales may slow.

AI search may change how people find your business.

A strong competitor may enter the market.

A supplier may increase prices.

A good opportunity may appear when cash is tight.

This is why I see budgeting as part of business thinking, not just bookkeeping.

I help people make better business decisions through psychology, strategy, and practical thinking. From that point of view, a budget is a way to test assumptions before reality tests them for you.

And reality, as we know, does not always mark gently…

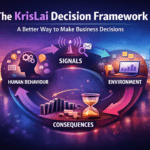

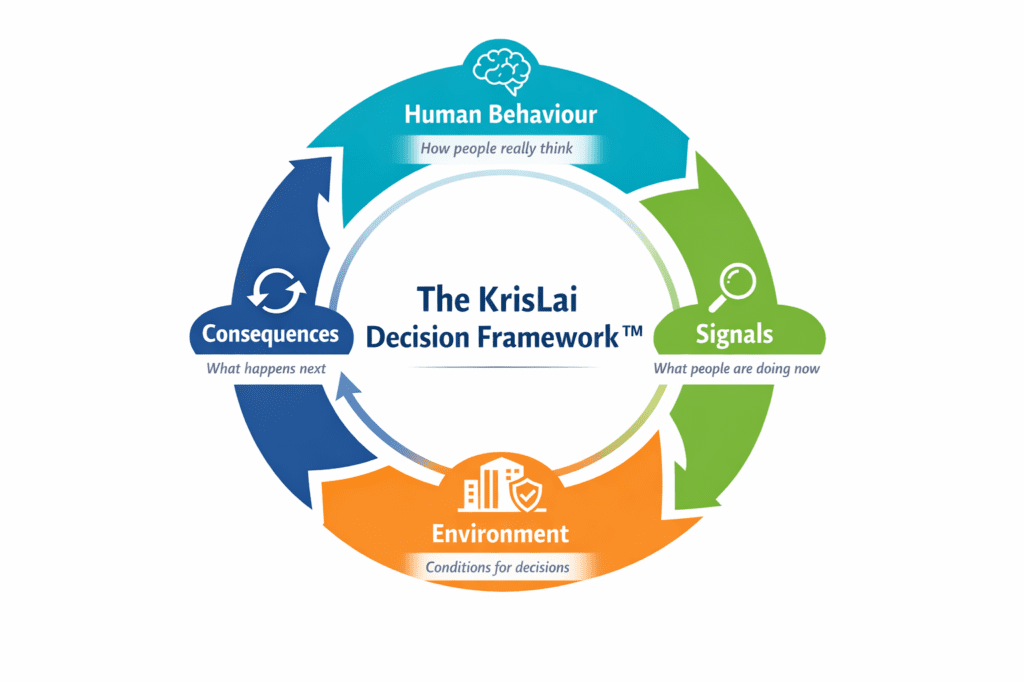

The KrisLai Decision Framework™ and small business budgeting

Small business budgeting fits naturally into this framework.

Human behaviour asks: How do owners, customers, staff, and suppliers actually behave?

Signals ask: What are revenue, margins, enquiries, costs, cash flow, and customer demand telling us?

Environment asks: Are supplier costs, seasonality, competition, capacity, and search behaviour changing?

Consequences ask: What happens if our budget assumptions are wrong?

This approach is part of the KrisLai Decision Framework, a practical method for improving business decisions.

Better decisions come from understanding behaviour, signals, environment, and consequences.

A practical model for better business decisions in complex environments. It focuses on four essential elements:

- Human Behaviour — how people actually think and decide

- Signals — what people are trying to do right now

- Environment — whether the system supports good decisions

- Consequences — what happens next, and after that

Strong decisions consider all four — not just one.

What should a small business budget include?

A small business budget should include expected revenue, fixed costs, variable costs, one-off costs, tax, debt payments, cash reserves, planned investment, and review points.

Here is a simple way to think about it:

| Budget category | What to include | Why it matters |

|---|

| Revenue | Sales, service income, recurring income | Shows expected money in |

| Fixed costs | Rent, salaries, insurance, software | Shows your baseline cost |

| Variable costs | Materials, delivery, commission, job costs | Shows the cost of activity |

| One-off costs | Equipment, repairs, setup costs | Prevents nasty surprises |

| Tax and VAT | Tax liabilities, VAT timing, accountant costs | Protects cash |

| Debt | Loan repayments, credit card costs, finance payments | Shows obligations |

| Reserves | Emergency fund and cash buffer | Reduces panic |

| Growth spend | Marketing, hiring, training, tools | Connects budget to strategy |

| Review points | Monthly checks, variance triggers, action dates | Turns the budget into a management tool |

A small business budget should show expected income, planned expenses, cash needs, tax obligations, debt payments, reserves, and the decision points where you will review performance.

If the budget only lists costs, it is incomplete. A useful budget should help you decide what to do next.

Why small business budgets fail

Small business budgets often fail because they are based on hope, costs are underestimated, cash flow is ignored, personal and business money are mixed, or the budget is not reviewed regularly.

This is the part many owners recognise.

The budget may look neat in January.

By April, reality has started editing it.

And reality is rarely polite!

1. The budget is built on hope, not evidence

This happens when the budget starts with what the owner wants to happen, rather than what the evidence suggests is likely.

Hope is useful.

Hope gets people moving.

But hope is not a revenue forecast.

A stronger budget uses:

last year’s numbers

current pipeline

customer behaviour

seasonal patterns

confirmed work

realistic conversion rates

cost trends

market signals

2. Personal and business finances are mixed

This is one of the quickest ways to make a small business budget confusing.

If personal spending and business spending are mixed, it becomes harder to see whether the business is really performing well.

It also makes tax, cash flow, and decision-making messier than necessary.

Separate accounts make the picture clearer.

Clearer numbers support better decisions.

3. Costs are underestimated

Many budgets include the obvious costs.

They miss the boring little ones.

Boring little costs are dangerous because they do not look important.

Then they gather in a group and become very important indeed.

Commonly missed costs include:

software subscriptions

insurance increases

bank charges

fuel

repairs

training

rework

waste

professional fees

website costs

marketing tools

equipment maintenance

card payment fees

4. Cash flow is confused with profit

Profit and cash are connected, but they are not the same thing.

A business can be profitable on paper and still struggle with cash if customers pay late, stock is bought early, or costs are due before income arrives.

That is why a budget should be connected to a cash flow forecast.

Useful related reading:

Cash Flow Forecasting as an Early-Warning Decision Tool

5. The budget is never reviewed

This is a big one.

Some businesses create a budget once, then file it away.

That is not budgeting!

That is ceremonial spreadsheet ownership.

A budget that is not reviewed is not a management tool.

It is a file with good intentions.

6. No one asks what changed

A budget becomes useful when you compare it with actual results.

If income is lower than expected, why?

If costs are higher, why?

If cash is tighter, why?

If marketing spend is up but leads are flat, why?

The question “what changed?” is where the decision value begins.

7. The budget does not connect to decisions

If the budget does not help you decide what to do, it becomes admin.

A good budget should help you decide whether to:

cut costs

raise prices

pause spending

invest more

hire carefully

change supplier

reduce low-margin work

increase marketing

protect cash

change the plan

A budget becomes dangerous when leaders treat it as a fixed promise instead of a working decision tool.

The aim is not to predict the year perfectly. The aim is to spot when reality starts moving away from the plan, then act early.

What this looks like in real business

Imagine a small service business creates an annual business budget in January.

The owner expects steady monthly income.

The budget includes rent, wages, fuel, software, insurance, and marketing.

So far, sensible.

But the budget misses a few things.

March and August are usually slower months.

Two major customers often pay late.

Supplier prices are rising.

A new marketing campaign may take three months to produce results.

Extra labour will be needed if the business wins more work.

By month four, the business is busy.

But cash is tight.

The owner feels confused because sales look healthy.

The problem is not lack of work.

The problem is timing, weak assumptions, and no monthly review.

This is what I have seen many times in real business. The headline number looks fine, but the warning signs are underneath.

The budget should have shown the pressure earlier.

The decision should have happened before the stress.

That is the difference between a budget as a document and a budget as an early-warning decision tool.

A business can be busy and still be under pressure. A good budget helps you see whether sales, costs, cash timing, and capacity are working together — or quietly pulling apart.

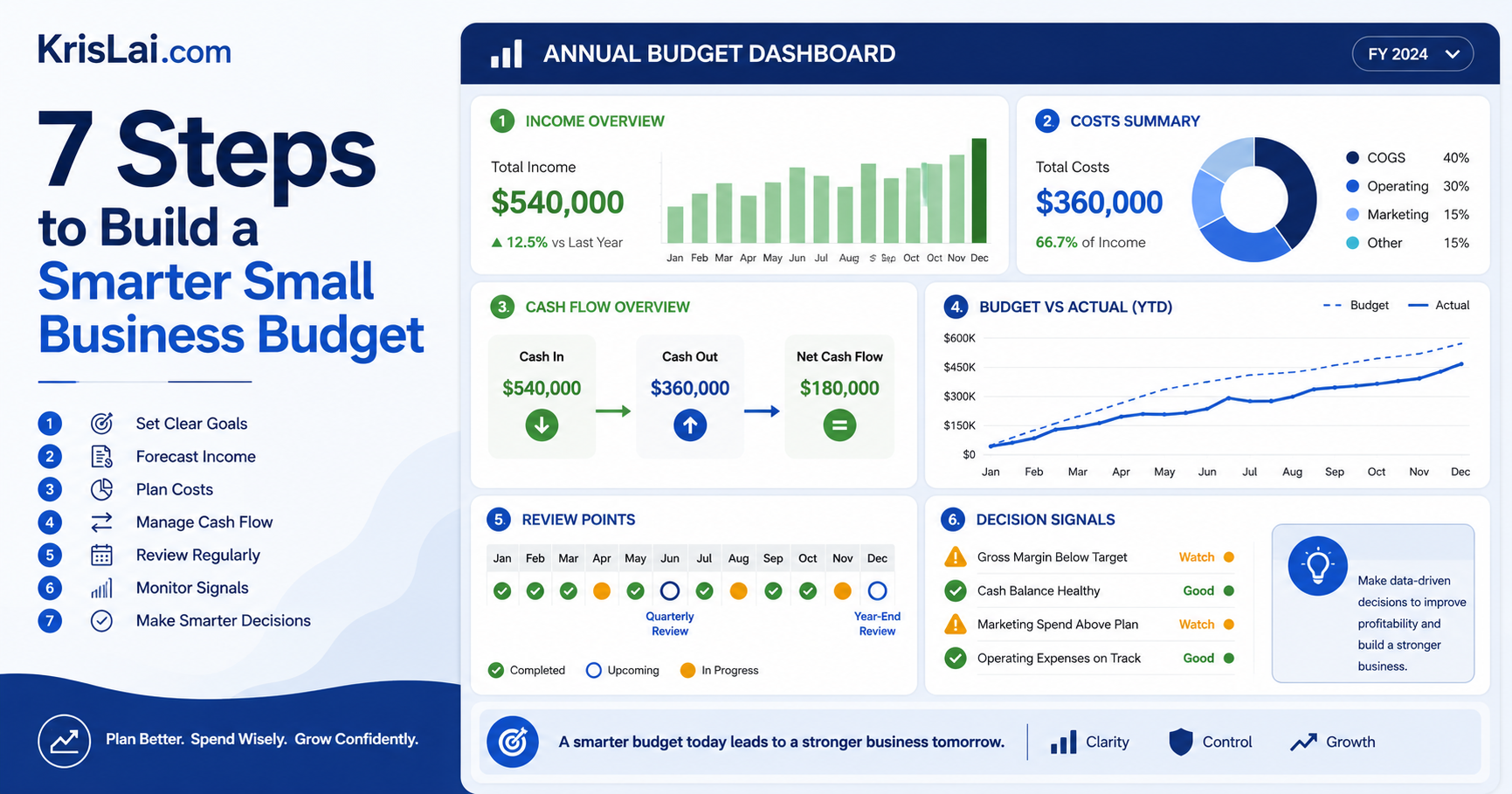

7 steps to build a smarter small business budget

To create a small business budget, review past numbers, set clear goals, forecast revenue, list costs, include cash timing, build scenarios, and review the budget monthly.

This is the practical process I recommend.

Step 1: Review last year’s numbers

Start by looking backwards before you plan forwards.

Review:

total income

monthly revenue

best and worst months

fixed costs

variable costs

one-off costs

gross margin

profit

cash flow

late payments

tax and VAT

debt repayments

unexpected costs

Look for patterns.

Which months were strong?

Which months were weak?

Which costs increased?

Which products or services produced good margin?

Which customers were slow to pay?

Which campaigns actually worked?

This step gives your budget evidence.

Without evidence, the budget becomes a motivational poster with numbers.

Step 2: Set clear business goals

Before building the budget, decide what the business is trying to achieve.

Are you trying to:

protect cash?

increase profit?

reduce debt?

hire staff?

buy equipment?

launch a new service?

increase marketing?

improve margin?

prepare for slow months?

build a cash reserve?

grow carefully?

The budget should support the goal.

If the goal is survival, the budget should protect cash.

If the goal is growth, the budget should show where investment is needed.

If the goal is better profit, the budget should focus on margin, cost control, and customer quality.

I write about how better decisions are made in business — combining strategy, behaviour, and practical thinking. Budgeting is one of the clearest examples of that.

The numbers should support the strategy.

Not the other way round.

Step 3: Forecast revenue realistically

A revenue forecast for a small business should be based on evidence, not just ambition.

Use:

past sales

current enquiries

confirmed work

customer intent

seasonal demand

repeat customers

conversion rates

average order value

market changes

search behaviour

sales pipeline

This is where customer behaviour matters.

A business may want higher sales, but customers still need a reason to buy.

They may also search differently now. Many people compare options through Google, YouTube, reviews, social media, AI tools, and direct recommendations before they contact a business.

So your budget should not assume demand just because the business wants growth.

Ask:

Are customers already showing buying signals?

Are enquiries increasing?

Are people searching for this problem?

Are competitors more visible?

Are AI tools changing how people compare options?

Are we answering the questions customers ask before they buy?

Useful related reading:

Customer Intent Marketing: How to Turn Buying Signals Into Sales

Step 4: List fixed, variable, and one-off costs

Separate costs properly.

This is important because different costs behave differently.

Fixed costs

Fixed costs stay broadly the same even if sales change.

Examples:

rent

salaries

insurance

software

phone and internet

vehicle finance

accountancy

licences

subscriptions

basic marketing retainers

Variable costs

Variable costs rise or fall with activity.

Examples:

stock

materials

delivery

payment fees

sales commission

job supplies

fuel for delivery

contractor costs

packaging

direct labour

One-off costs

One-off costs do not happen every month, but they still need planning.

Examples:

equipment

repairs

website redesign

training

new software setup

legal fees

large insurance payments

vehicle repairs

office move

Do not ignore one-off costs because they are not monthly.

They are often the ones that arrive at the worst possible moment, wearing a little hat labelled “surprise!”

Many small business budgets fail because costs are underestimated. The obvious costs are included, but the smaller costs are ignored until they build into a real cash problem.

Step 5: Build in cash flow and timing

A budget shows expected income and expenses.

Cash flow shows when money enters and leaves the bank account.

You need both.

For example:

You may invoice in March.

The customer may pay in May.

Wages may be due in April.

VAT may be due before the cash feels comfortable.

A supplier may need payment before your customer pays you.

This is why a business can look profitable but still feel cash-poor.

When building the annual budget, include timing.

Ask:

When will customers pay?

When are wages due?

When is VAT due?

When are loan payments due?

When do large supplier bills arrive?

When are the slow months?

When do we need extra stock?

When will marketing spend produce results?

A budget without timing can create false comfort.

Step 6: Add scenarios and reserves

A smart small business budget should include more than one version of the future.

Do not build one perfect budget and pretend the year will behave.

It probably will not.

Build three scenarios:

cautious

expected

optimistic

Cautious scenario

This is your pressure test.

What happens if:

sales are lower?

costs are higher?

customers pay later?

a key client leaves?

marketing takes longer?

Expected scenario

This is your most realistic view based on current evidence.

It should not be gloomy.

It should not be heroic.

It should be honest.

Optimistic scenario

This shows what may happen if things go well.

Use it carefully.

Optimism is useful when it inspires action.

It becomes dangerous when it starts approving spending on its own.

Also build a reserve.

A small business emergency fund gives you room to breathe when reality changes.

A common aim is to build towards three to six months of essential operating costs, although the right amount depends on your industry, cash flow, seasonality, and risk.

Step 7: Turn the budget into a monthly decision tool

This is the step many businesses miss.

The budget is not finished when the spreadsheet is complete.

That is when the useful work begins.

Review the budget each month.

Compare:

budget vs actual revenue

budget vs actual costs

gross margin

cash position

late payments

marketing spend

conversion rates

stock levels

staff capacity

customer demand

supplier cost changes

Then ask:

What changed?

Why did it change?

Is this temporary or a trend?

What decision should we make now?

This is how an annual budget becomes an early-warning decision tool.

Plan → Forecast → Spend → Review → Variance → Decision → Adjust → Plan

A budget should not be a one-off spreadsheet. It should be a loop that helps leaders notice change, make better decisions, and adjust before problems grow.

Budget vs cash flow forecast: what is the difference?

A budget sets expected income and expenses, while a cash flow forecast shows when money is expected to enter and leave the business bank account.

Both are useful.

They do different jobs.

| Budget | Cash flow forecast |

| Plans income and expenses | Tracks timing of cash |

| Helps set targets | Helps avoid cash shortfalls |

| Shows expected profit or loss | Shows bank balance pressure |

| Often reviewed monthly or quarterly | Often checked weekly or monthly |

| Helps plan spending | Helps protect survival |

A budget may show that the business should make profit this year.

A cash flow forecast may show that April will still be painful.

That matters.

Painful Aprils have a habit of arriving whether or not the annual budget looked elegant!

Monthly budget review: the part many businesses skip

A monthly budget review compares planned figures with actual results so leaders can spot problems early and make better decisions.

This review does not need to be complicated.

Each month, check:

Revenue: Did we hit the sales target?

Gross margin: Are we making enough from each sale?

Fixed costs: Did regular costs stay under control?

Variable costs: Did delivery costs rise?

Cash: Is the bank position healthy?

Debtors: Are customers paying on time?

Marketing: Is spend producing useful leads?

Capacity: Can the team handle the work?

Stock: Are we holding too much or too little?

Customer demand: Are enquiries rising or falling?

Search behaviour: Are people still finding us in the same way?

The value of the budget is not in creating it.

The value is in reviewing it.

A monthly budget review should not be a blame session. It should be a learning session. The question is not “Who got this wrong?” The better question is “What has changed, and what should we do next?”

Budget variance: what changed and why?

Budget variance is the difference between what you planned and what actually happened.

There are two main types.

A favourable variance is when the result is better than expected.

An unfavourable variance is when the result is worse than expected.

But the label is not enough.

You need to understand why the variance happened.

For example:

Revenue may be below budget because enquiries fell.

Revenue may be below budget because conversion fell.

Revenue may be below budget because customers delayed decisions.

Costs may be above budget because suppliers increased prices.

Costs may be above budget because of waste, rework, or poor planning.

Cash may be below forecast because customers paid late.

Marketing may be over budget because lead quality dropped.

The useful question is:

What is the variance telling us?

Then ask:

Is this a one-off?

Is this a trend?

Is this in our control?

Do we need to change price?

Do we need to reduce cost?

Do we need to adjust marketing?

Do we need to protect cash?

Do we need to review the business model?

This is where budgeting becomes leadership.

How to use a budget as an early-warning decision tool

A budget becomes an early-warning decision tool when you use it to spot weak signals, compare actual results with expectations, and act before small problems become serious.

This is the central idea of this article.

Do not use the budget only to ask:

Did we hit the number?

Use it to ask:

What is changing?

What are the signals?

What behaviour are we seeing?

What pressure is building?

What consequence may come next?

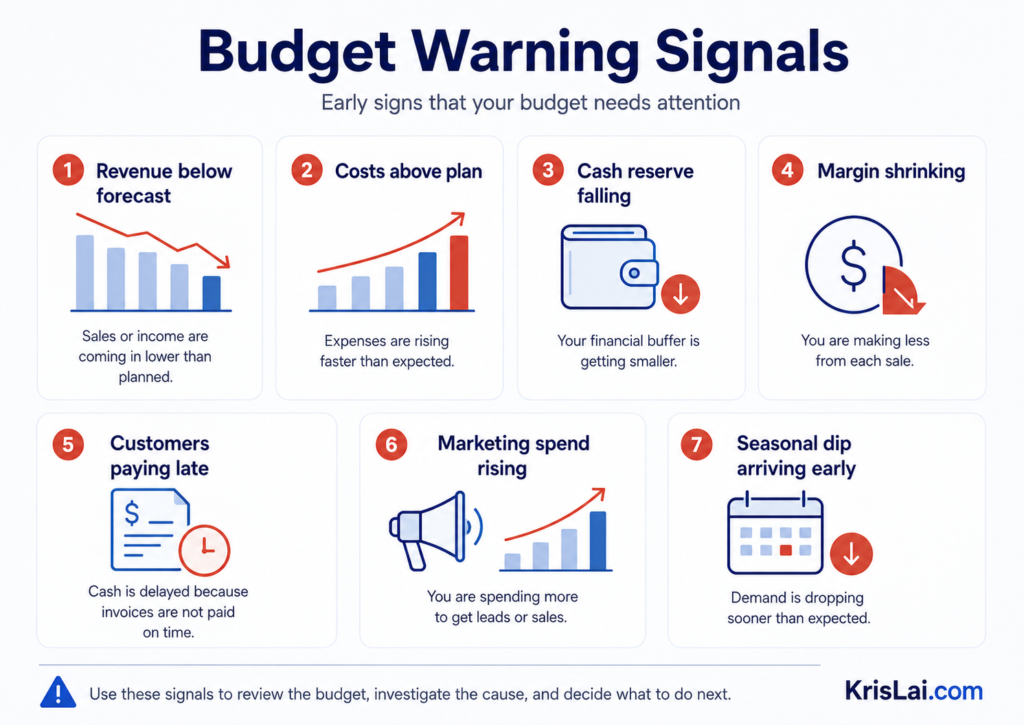

Set review triggers.

Here are some of the clearest warning signals that tell you your budget needs attention before a small issue becomes a bigger problem:

Budget Warning Signals highlights the signs that a small business budget may need review, adjustment, or a change in decision.

For example:

Revenue is 10% below forecast.

Costs are 10% above budget.

Cash reserve falls below target.

Gross margin drops.

Debtor days rise.

Marketing spend rises but leads do not improve.

Staff overtime increases.

Supplier costs rise.

Seasonal dip starts earlier than expected.

Customer enquiries shift from Google to AI-assisted search.

These are not just finance notes.

They are decision signals.

Over time, I’ve found that good decisions rarely come from data alone. They come from understanding people, reading signals, creating the right environment, and thinking beyond the immediate outcome.

A budget becomes more useful when you connect each number to a possible action. If this number changes, what decision should follow?

Small business budgeting under uncertainty

Small business budgeting under uncertainty means building a budget that can adapt when costs, demand, cash flow, or market conditions change.

This matters because the year rarely follows the plan.

That does not mean planning is pointless.

It means planning should be flexible.

Instead of building one fixed budget, build a budget with adaptation points.

Use:

cautious, expected, and optimistic scenarios

monthly reviews

cash reserve targets

spending limits

decision triggers

variance checks

regular updates

This connects with modern decision methods such as scenario planning and adaptive planning, but it does not need to sound academic.

For a small business, the practical version is simple:

If sales fall below this level, what do we do?

If costs rise above this level, what do we do?

If cash drops below this level, what do we do?

If demand improves, when do we invest?

If a campaign underperforms, when do we stop?

If customer behaviour changes, how quickly do we adapt?

That is real-world strategy.

Not textbook strategy.

Budgeting and AI search behaviour

AI is changing how customers find answers.

People may now ask tools like ChatGPT, Gemini, Claude, Perplexity, or Google AI Overviews to compare options before visiting a business website.

This matters for budgeting because your revenue forecast depends on customer behaviour.

If your budget assumes more sales, you need to ask:

Where will those customers come from?

Are they still using Google in the same way?

Are they asking AI tools for recommendations?

Are they comparing suppliers before they contact you?

Are your articles, service pages, and reviews visible enough?

Are you answering the questions customers ask before buying?

This is why AI and changing search behaviour affect budgeting.

A budget should not assume demand without checking the signals.

Useful related reading:

How AI Is Changing Search Behaviour

Should you use a business budget template, spreadsheet, or accounting software?

A business budget template or spreadsheet is useful for getting started, while accounting software is better when you need live data, automation, and regular reporting.

Use Excel or Google Sheets if:

your budget is simple

you want flexibility

you are still learning

you want to test scenarios

you want a low-cost starting point

Use accounting software if:

you need regular reporting

you want fewer manual errors

you have more transactions

you need better cash flow visibility

you want easier budget vs actual tracking

you work with an accountant

Use a template if:

you want structure

you are not sure where to start

you need prompts for categories

you want to avoid missing key costs

The best tool is the one you will actually use.

A perfect budgeting system that nobody updates is just digital furniture.

Start with a simple budget spreadsheet if that helps you take action. You can move to accounting software later when the business needs more automation, reporting, and live data.

What you should actually do

Here is the simple version:

Build one annual budget.

Break it into months.

Use realistic revenue assumptions.

Separate fixed, variable, and one-off costs.

Include cash flow timing.

Build cautious, expected, and optimistic scenarios.

Set a cash reserve target.

Review actual results every month.

Investigate budget variance.

Set decision triggers.

Update the budget when reality changes.

The aim is not to predict the year perfectly.

The aim is to notice when reality starts moving away from the plan.

If you notice any of the warning signals shown above, do not ignore them. Review the numbers, investigate the cause, and decide what action needs to follow.

A small business budget works best when it is connected to cash flow, break-even analysis, financial trend analysis, and customer demand signals.

In other words, do not treat the budget as a lonely spreadsheet. Treat it as part of a wider decision system.

Useful related reading:

Break-Even Analysis for Smarter Decisions

Financial Dashboards That Help Leaders Make Better Decisions

Small business budget checklist

Before you finalise your annual business budget, ask:

Have we reviewed last year’s numbers?

Have we separated business and personal spending?

Have we forecast revenue realistically?

Have we included fixed costs?

Have we included variable costs?

Have we included one-off costs?

Have we planned for tax and VAT?

Have we included debt repayments?

Have we allowed for slow months?

Have we built a cash reserve?

Have we created cautious, expected, and optimistic scenarios?

Have we set monthly review dates?

Have we defined budget variance triggers?

Have we connected the budget to real business decisions?

Have we asked what happens if our assumptions are wrong?

If the answer to several of these is no, the budget needs more work.

That is not failure.

That is exactly why the checklist exists!

Want to turn this article into action? Download the free Small Business Budget Checklist.

Use it to check your revenue assumptions, fixed costs, variable costs, cash flow timing, reserves, monthly reviews, and decision triggers before finalising your annual budget.

KrisLai Decision Insight

This connects closely to how I think about decisions more broadly in the KrisLai Decision Framework™.

A small business budget helps leaders think through:

Behaviour: How owners spend, customers buy, and teams respond.

Signals: What revenue, costs, margins, cash flow, and demand are telling you.

Environment: How suppliers, seasonality, competition, capacity, and AI search behaviour are changing.

Consequences: What happens if costs rise, sales fall, cash tightens, or assumptions prove wrong.

The numbers matter.

But the decisions around the numbers matter even more.

I write about how better decisions are made in business — combining strategy, behaviour, and practical thinking.

A budget is one of the simplest ways to bring those ideas into everyday business management.

FAQ

What is a small business budget?

A small business budget is a financial plan that estimates income, expenses, cash needs, and planned spending over a set period.

How do I create a small business budget?

Start with past financial data, forecast revenue, list fixed and variable costs, include one-off expenses, add cash flow timing, build in reserves, and review the budget monthly.

What should be included in a small business budget?

A small business budget should include revenue, fixed costs, variable costs, one-off costs, tax, debt repayments, reserves, growth spending, and review points.

Why is budgeting important for small businesses?

Budgeting helps small businesses control costs, manage cash flow, prepare for slow months, plan growth, and make better decisions.

What is the difference between a budget and a cash flow forecast?

A budget sets expected income and expenses. A cash flow forecast shows when money is expected to enter and leave the bank account.

How often should I review my business budget?

Review the full budget monthly and check short-term cash flow weekly if cash is tight or the business is growing quickly.

What is budget variance?

Budget variance is the difference between what you planned and what actually happened.

Why do small business budgets fail?

Small business budgets often fail because they are based on hope, costs are underestimated, cash flow is ignored, personal and business spending are mixed, or the budget is not reviewed.

Can I use Excel for a small business budget?

Yes. Excel or Google Sheets can work well for simple budgets, especially when starting out. As the business grows, accounting software may make tracking easier.

How much should a small business keep as an emergency fund?

A common goal is to build towards three to six months of essential operating costs, though the right amount depends on cash flow, seasonality, and risk.

Research and experience note

This article is based on practical business experience, independent research, and analysis of how small business budgets are used in real decision-making.

Useful reference sources include:

Xero: How to Create a Small Business Budget

SumUp: Small Business Budget Guide

Federation of Small Businesses: How to Create a Small Business Budget

Capsule CRM: How to Create and Manage a Small Business Budget

U.S. Chamber: Budgeting for Small Business

The aim is not to make budgeting more complicated.

The aim is to make it more useful.

Small business budgeting connects closely to wider business thinking. These articles may help you go deeper:

Conclusion and Final Thoughts

If you remember nothing else from this article, remember this:

Start with this one thing: build your budget, then review it every month by asking, “What changed, why did it change, and what should we do next?”

That single question turns a budget from a spreadsheet into a decision tool.

It helps you notice weak signals.

It helps you protect cash.

It helps you plan growth more carefully.

It helps you avoid being surprised by problems that were already starting to appear.

Small business budgeting is not about controlling every penny for the sake of it.

It is about creating enough clarity to make better choices before pressure builds.

Better decisions always come from understanding behaviour, signals, environment, and consequences.

If you want a practical way to think through business decisions, download my free KrisLai Decision Framework™ guide.

It will help you look at decisions through four simple lenses: behaviour, signals, environment, and consequences.

Use it before major choices about strategy, customers, marketing, operations, finance, and AI.

If you enjoy exploring the ideas behind better business decisions, you may find the Business Thinking Hub useful.

About the author

Kris Lai is a business operator and managing director with experience in land and building surveying, facilities management, logistics, and service delivery.

Earlier in his career, he worked as a Search Engine Evaluator (via Lionbridge, supporting Google), where he assessed search result relevance, user intent, and content quality using structured evaluation frameworks. This experience gives him a rare, practical understanding of how search systems interpret signals and make ranking decisions.

In parallel, whilst working with a charity organisation, he has delivered 1000’s of structured presentations in English, Finnish, and Chinese to audiences ranging from small groups to more than 600 people, and has spent decades mentoring and developing others. This experience informs his approach to clarity, communication, and decision-making under pressure.

He writes about AI, search behaviour, business strategy, and decision-making from a practical, real-world perspective.

👉 Explore ideas connected to better business decisions:

- How AI Is Changing Search Behaviour (And What Businesses Must Do Now)

- Decision-Making Framework Examples: The KrisLai Method in Action

- The KrisLai Decision Framework: A Better Way to Make Business Decisions

- Micro vs Macro Marketing: When to Target Broad Audiences vs Niche Customers

- Customer Intent Marketing: How to Turn Buying Signals Into Sales