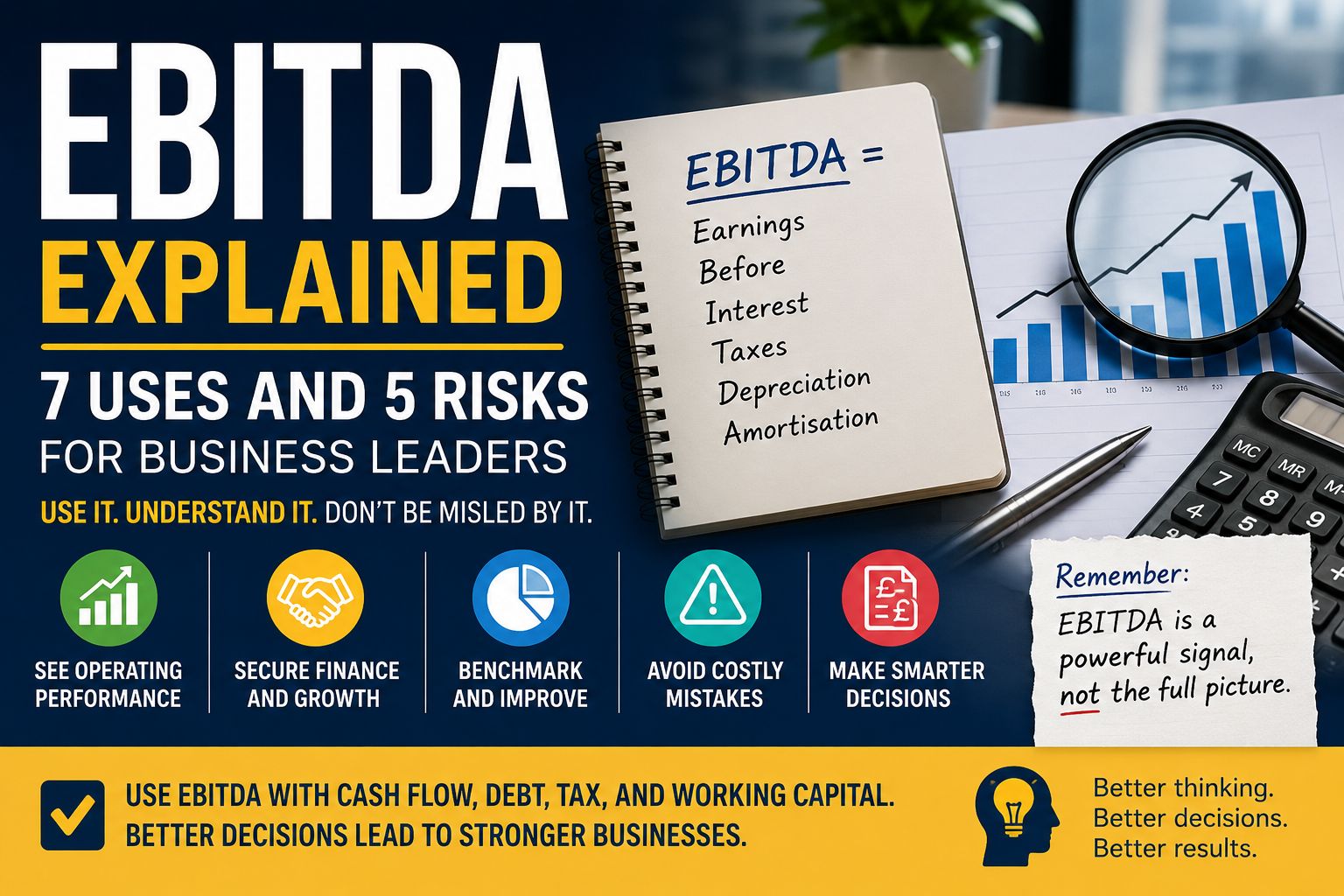

A practical guide to using EBITDA for finance, valuation, growth, and performance decisions — without mistaking it for cash flow.

EBITDA helps business leaders understand operating performance before interest, tax, depreciation, and amortisation. It can support finance, valuation, benchmarking, and growth decisions. But EBITDA can also mislead when leaders treat it as cash flow or ignore debt, tax, equipment costs, working capital, and future investment needs.

EBITDA is one of those finance terms that sounds more complicated than it needs to be.

It is useful. It is widely used. It can help with loans, valuations, investor conversations, and performance reviews.

But it can also make a business look healthier than it really is.

That is why EBITDA should not be treated as a magic number. It should be treated as a signal. A useful signal, yes — but still only one signal.

What this article covers

This article explains:

- what EBITDA means

- what EBITDA stands for

- how to calculate EBITDA

- EBITDA formula and worked example

- EBITDA margin

- what a good EBITDA margin means

- EBITDA vs net income

- EBITDA vs gross profit

- EBITDA vs EBIT

- EBITDA vs cash flow

- adjusted EBITDA

- EBITDA and business valuation

- EBITDA and business loans

- 7 decisions EBITDA can help with

- 5 ways EBITDA can mislead

- what leaders should use alongside EBITDA

Table of contents

- What is EBITDA?

- What does EBITDA actually tell you?

- How do you calculate EBITDA?

- What is EBITDA margin?

- What is a good EBITDA margin?

- EBITDA vs net income

- EBITDA vs gross profit

- EBITDA vs EBIT

- EBITDA vs cash flow

- 7 decisions EBITDA can help business leaders make

- 5 ways EBITDA can mislead leaders

- What is adjusted EBITDA?

- How is EBITDA used in business valuation?

- Why does a lender care about EBITDA?

- What this looks like in real business

- Where this goes wrong

- What you should actually do

- FAQ

- EBITDA stands for earnings before interest, taxes, depreciation and amortisation.

- EBITDA can help leaders understand operating performance before finance costs, tax, and some non-cash accounting costs.

- EBITDA is useful for finance, valuation, benchmarking, and performance reviews.

- EBITDA is not the same as cash flow, net profit, gross profit, or free cash flow.

- A business can have strong EBITDA and still struggle with debt, tax, slow-paying customers, stock, equipment costs, or cash flow.

- Use EBITDA alongside operating cash flow, debt payments, capital expenditure, tax, working capital, and future investment needs.

What is EBITDA?

EBITDA stands for earnings before interest, taxes, depreciation and amortisation. It is a financial measure that shows business profit before financing costs, tax, and some non-cash accounting costs. Leaders use EBITDA to compare operating performance, discuss finance, review valuation, and understand business strength before other costs are included.

In simpler words, EBITDA tries to show how much profit the core business is making before four things are taken out:

- interest

- tax

- depreciation

- amortisation

Those four items can vary a lot between businesses.

One business may have high debt.

Another may have little debt.

One may own expensive equipment.

Another may use very few fixed assets.

One may pay more tax because of its structure.

Another may have different tax timing.

EBITDA tries to remove some of that noise so leaders, lenders, buyers, and investors can look at the operating engine of the business.

The British Business Bank describes EBITDA as a standard measure banks may use to judge business performance and assess repayment ability. Investopedia also defines EBITDA as earnings before the impact of financing costs, taxes, and certain non-cash accounting charges.

EBITDA is a way of looking at business profit before interest, tax, depreciation, and amortisation are included.

It can help you see the strength of the core business, but it does not show the full financial picture.

What do the letters in EBITDA mean?

EBITDA stands for:

That sounds technical, but the idea is simple.

EBITDA asks:

How much profit does the business make from its main operations before finance structure, tax, and certain accounting costs affect the final number?

That is useful.

But it is not complete.

Think of EBITDA like checking the engine of a vehicle before looking at the fuel bill, road tax, loan payments, repair costs, and whether the tyres need replacing.

The engine matters. If the engine is weak, there is a problem.

But a strong engine does not mean the whole vehicle is cheap to run, safe to drive, or ready for a long journey.

EBITDA tells you something useful. It does not tell you everything.

Is EBITDA useful? Direct answer:

EBITDA is useful when you want to understand operating performance before interest, tax, depreciation, and amortisation. It can help with finance, valuation, benchmarking, and performance reviews. But EBITDA is incomplete because it does not show actual cash flow, debt repayments, tax payments, working capital, or capital expenditure.

That is the heart of the issue.

EBITDA is not bad.

Blindly relying on EBITDA is bad.

As the Swedish saying goes: “Lagom är bäst.” It means “the right amount is best.”

That is a good way to think about EBITDA.

Use it.

But do not overuse it.

Idea Bridge: from finance metric to business decision

Many people ask:

“Is EBITDA good or bad?”

That is not the best question.

A better question is:

“What decision are we using EBITDA to support?”

That changes the whole discussion.

EBITDA can help you think about:

- business loans

- valuation

- performance trends

- operational improvement

- growth plans

- cost control

- investor conversations

- acquisition offers

- debt capacity

But it should not be used alone!

In my experience, finance numbers become dangerous when leaders treat them as answers instead of signals.

EBITDA is a signal.

The decision still needs judgement.

What does EBITDA actually tell you?

EBITDA tells you how much profit the business generates from core operations before interest, tax, depreciation and amortisation. It is useful for comparing operating performance across periods or similar businesses. But it does not show final profit, cash in the bank, debt repayments, tax payments, or future investment needs.

EBITDA can help you understand whether the business model itself is generating profit.

For example, if revenue is growing but EBITDA is falling, that may signal rising costs, weak pricing, poor efficiency, or margin pressure.

If EBITDA is rising while revenue is flat, that may suggest better cost control, improved pricing, stronger productivity, or a better sales mix.

If EBITDA margin is falling, the business may be working harder but keeping less.

That is why EBITDA can be useful for leadership.

It helps you ask better questions.

It does not remove the need to ask them.

EBITDA can help you see operating performance

Operating performance means how well the core business works before finance, tax, and some accounting charges are included.

That can be useful when comparing:

- this year with last year

- one branch with another

- one product line with another

- one business with another similar business

- performance before and after a strategy change

- performance before and after cost increases

- performance before and after a pricing review

EBITDA is especially useful when businesses have different debt levels, tax positions, or asset accounting costs.

However, it should not become a comfort blanket.

A business can look good on EBITDA and still be financially stretched.

That is where leaders need caution.

How do you calculate EBITDA?

You can calculate EBITDA by adding interest, tax, depreciation, and amortisation back to net profit. You can also calculate it by taking operating profit and adding back depreciation and amortisation. Both methods aim to show earnings before finance costs, tax, and certain non-cash accounting charges.

There are two common ways to calculate EBITDA:

EBITDA formula 1

EBITDA = Net Profit + Interest + Tax + Depreciation + Amortisation

EBITDA formula 2

EBITDA = Operating Profit + Depreciation + Amortisation

The British Business Bank explains both routes: adding depreciation and amortisation to operating profit, or adding interest, tax, depreciation and amortisation back to net profit.

EBITDA = Net Profit + Interest + Tax + Depreciation + Amortisation

Or:

EBITDA = Operating Profit + Depreciation + Amortisation

EBITDA calculation example

Let’s use a simple example:

Revenue: £1,000,000

Operating costs before depreciation: £760,000

Depreciation: £40,000

Operating profit: £200,000

Interest: £25,000

Tax: £35,000

Net profit: £140,000

Using formula 1:

EBITDA = Net Profit + Interest + Tax + Depreciation + Amortisation

EBITDA = £140,000 + £25,000 + £35,000 + £40,000 + £0

EBITDA = £240,000

Using formula 2:

EBITDA = Operating Profit + Depreciation + Amortisation

EBITDA = £200,000 + £40,000 + £0

EBITDA = £240,000

Same answer.

Different route.

And thankfully, no need to pretend this is more mysterious than it is!

Step-by-step EBITDA calculation

- Start with net profit or operating profit.

- Add back interest if starting from net profit.

- Add back tax if starting from net profit.

- Add back depreciation.

- Add back amortisation.

- Check that the result makes sense.

- Compare it with cash flow before making a decision.

That last step matters.

Calculating EBITDA is simple.

Using it wisely is the real skill.

What is EBITDA margin?

EBITDA margin shows EBITDA as a percentage of revenue. It helps leaders see how much operating profit the business keeps from each pound of sales before interest, tax, depreciation and amortisation. EBITDA margin is useful for comparing performance over time or against similar businesses.

The formula is:

EBITDA margin = EBITDA ÷ Revenue × 100

Using the earlier example:

EBITDA = £240,000

Revenue = £1,000,000

EBITDA margin = £240,000 ÷ £1,000,000 × 100

EBITDA margin = 24%

That means the business keeps 24p of EBITDA for every £1 of revenue.

Xero’s UK glossary explains EBITDA margin in a similar way: it shows EBITDA as a percentage of total revenue and helps show how much of each pound becomes operational profit.

Why EBITDA margin matters

EBITDA margin is useful because it shows the relationship between profit and revenue.

Revenue alone can mislead.

A business can grow sales and still become weaker if costs rise faster than income.

For example:

- revenue rises by 20%

- staff costs rise by 30%

- fuel costs rise by 25%

- admin costs rise by 15%

- EBITDA margin falls

That business is busier.

But not necessarily stronger.

This is where leaders need to look beyond the excitement of sales growth.

Turnover is vanity, profit is sanity, and cash is reality.

It is an old saying, but it has survived because it is painfully true.

What is a good EBITDA margin?

A good EBITDA margin depends on industry, business model, size, growth stage, pricing power, capital needs, debt, and cash flow. A 20% or 30% EBITDA margin may be strong in some sectors, but it should always be compared with similar businesses and your own trend over time.

There is no universal “good” EBITDA margin.

That answer may be annoying!

But it is also true.

A software business, cleaning contractor, manufacturer, delivery business, consultancy, hotel, retailer, and facilities management business may all have very different margin expectations.

What matters is context.

Ask:

- Is our EBITDA margin improving or falling?

- How does it compare with similar businesses?

- Are we pricing properly?

- Are costs rising faster than revenue?

- Are we relying on one customer?

- Is cash flow also improving?

- Are we investing enough for the future?

- Are we ignoring equipment replacement?

- Is the margin sustainable?

A 30% EBITDA margin may look excellent.

But if customers are paying late, debt repayments are heavy, tax is due, and equipment needs replacing, the real decision is more complicated.

This is why I rarely like single-number thinking.

It feels efficient.

But it can hide risk.

A high EBITDA margin is useful only if the business can also turn profit into cash, manage debt, pay tax, fund working capital, and invest in the assets it needs.

A strong margin is a good sign. It is not a full health check.

EBITDA vs net income: what is the difference?

Net income shows profit after all costs, while EBITDA adds back interest, tax, depreciation and amortisation to show operating profit before those items. EBITDA is useful for comparing operating performance. Net income is useful for understanding final profit after finance, tax, and accounting costs.

Both numbers matter.

They simply answer different questions.

EBITDA asks:

How strong is the core operation before interest, tax, depreciation, and amortisation?

Net income asks:

What profit is left after all those costs?

Here is a simple comparison:

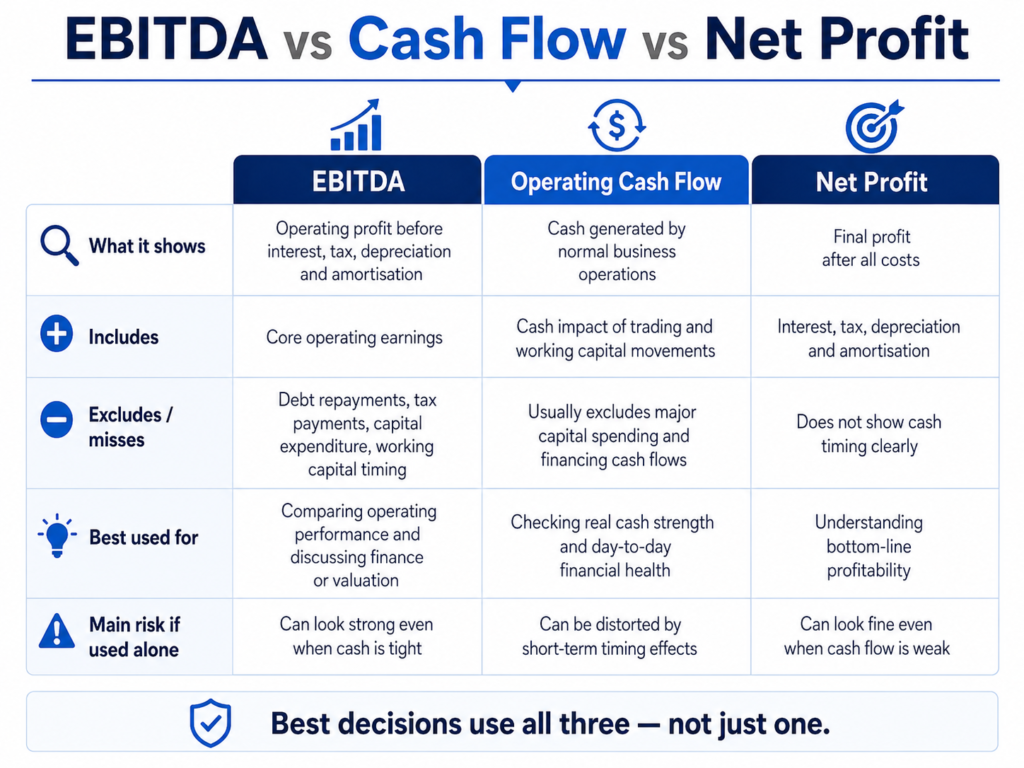

| Metric | What It Shows | Best Used For |

|---|---|---|

| EBITDA | Operating profit before interest, tax, depreciation, and amortisation | Comparing operating performance |

| Net income | Final profit after all costs | Understanding bottom-line profitability |

Investopedia explains that EBITDA adds interest, taxes, depreciation, and amortisation back to earnings, while net income is after those costs.

When EBITDA is higher than net income

EBITDA is often higher than net income because it adds costs back.

That is not automatically wrong.

It just means you need to understand what has been removed.

For example, a business with high debt may show healthy EBITDA but much lower net income after interest.

A business with expensive equipment may show healthy EBITDA but lower net income after depreciation.

That is why EBITDA can help comparison, but it can also flatter performance.

Is EBITDA the same as gross profit?

No. Gross profit shows revenue after direct costs, such as materials, labour, or cost of sales. EBITDA shows broader operating earnings before interest, tax, depreciation and amortisation. Gross profit focuses on direct margin. EBITDA gives a wider view of operating performance after more business costs.

Gross profit is usually calculated like this:

Gross Profit = Revenue – Cost of Sales

EBITDA is calculated later in the profit structure.

It includes more operating costs than gross profit, but excludes interest, tax, depreciation, and amortisation.

Here is the difference:

| Metric | Focus | Useful Question |

|---|---|---|

| Gross profit | Revenue after direct costs | Are we pricing and delivering profitably? |

| EBITDA | Operating earnings before interest, tax, depreciation, and amortisation | Is the wider operation generating profit? |

Investopedia describes gross profit as revenue minus cost of goods sold, while EBITDA measures operational profitability by excluding financing, tax, and certain non-cash costs.

Why this difference matters

Gross profit can look strong while EBITDA is weak.

That may happen if overheads are too high.

For example:

- direct job margin is good

- office costs are high

- admin team is overloaded

- software costs have grown

- management costs have increased

- vehicle costs are rising

- marketing costs are not converting

In that case, the business may sell profitably at job level but lose strength at operating level.

That is useful to know.

It tells the leader where to look next.

EBITDA vs EBIT: which is better?

EBIT includes depreciation and amortisation, while EBITDA adds them back. EBITDA can help compare operating performance before asset-ageing costs. EBIT may be better for asset-heavy businesses because it includes depreciation and gives more weight to equipment, vehicles, plant, and other long-term assets.

EBIT stands for earnings before interest and taxes.

It does not add back depreciation and amortisation.

That means EBIT may give a more cautious view for businesses that rely on expensive assets.

For example:

- delivery businesses with vans

- cleaning businesses with machines

- manufacturing businesses with equipment

- construction firms with plant

- hotels with buildings and fixtures

- facilities companies with specialist tools

Development Bank of Wales notes that EBIT may be a better measure for asset-intensive businesses because EBITDA ignores capital expenditure.

When EBIT may be more useful

EBIT may be more useful when physical assets matter heavily.

If the business needs regular vehicle replacement, machinery, equipment, refurbishment, or IT infrastructure, then ignoring depreciation can make performance look too clean.

EBITDA may say:

“The operation looks strong.”

EBIT may say:

“Yes, but the assets are wearing out.”

That second sentence matters.

Especially when the next equipment bill arrives wearing steel-capped boots.

EBITDA vs cash flow: why this matters

EBITDA is not cash flow because it does not include working-capital movements, debt repayments, tax payments, capital expenditure, or delayed customer payments. A business can show strong EBITDA and still have weak cash flow if money is tied up in invoices, stock, assets, or debt.

This is the most important section for many business owners.

EBITDA can be positive while cash flow is poor.

That happens because EBITDA does not fully capture:

- customers paying late

- stock increasing

- suppliers needing payment

- VAT or tax due

- loan repayments

- equipment purchases

- vehicle finance

- owner drawings

- dividends

- capital expenditure

- working capital pressure

Operating cash flow is different because it looks at cash generated by core operations and adjusts for working capital movements. Investopedia explains that operating cash flow includes changes in working capital, while EBITDA does not.

Free cash flow goes further by considering capital expenditure. Investopedia describes free cash flow as cash remaining after operating expenses and capital expenditure.

A business can have strong EBITDA and still run out of cash.

This can happen when customers pay late, stock increases, debt repayments are heavy, tax is due, or equipment needs replacing.

Use EBITDA with operating cash flow, working capital, debt payments, tax, and capital expenditure before making major decisions.

To make the difference clearer, here is a simple comparison of EBITDA, cash flow, and net profit:

The main lesson is simple: each metric tells you something useful, but the best decisions come from using all three together rather than relying on just one.

Simple example: strong EBITDA, weak cash

A business has:

- EBITDA: £180,000

- tax due: £35,000

- loan repayments: £60,000

- new equipment needed: £45,000

- overdue customer invoices: £90,000

- rising stock: £40,000

On paper, EBITDA looks good.

In reality, cash is tight.

That does not mean EBITDA is useless.

It means EBITDA is incomplete.

And incomplete numbers can lead to incomplete decisions.

7 decisions EBITDA can help business leaders make

EBITDA can help business leaders make decisions about operating performance, finance readiness, borrowing capacity, valuation, efficiency, benchmarking, and growth. It works best when used as one signal alongside cash flow, debt, tax, capital expenditure, working capital, customer risk, and future scenarios.

Let’s look at the seven best uses…

1. Are operations becoming more profitable?

EBITDA helps show whether the core business is becoming more profitable before interest, tax, depreciation and amortisation are included.

This is useful when looking at trends.

Compare EBITDA over time:

- this month vs last month

- this quarter vs last quarter

- this year vs last year

- before and after a pricing change

- before and after cost increases

- before and after a restructuring

- before and after a new contract

If EBITDA is rising, the operation may be getting stronger.

If EBITDA is falling, the business may have cost pressure, pricing issues, weak productivity, or margin erosion.

The next question is:

Why?

That is where leaders must go deeper.

2. Can we compare performance across periods?

EBITDA helps compare performance across periods because it removes some items that may vary due to finance structure, tax, or asset accounting.

For example, one year may include higher interest costs because the business took on debt.

Another year may include more depreciation because of new equipment.

EBITDA can help leaders see whether the underlying operation improved or weakened.

But keep the comparison fair.

Use the same calculation method.

Check unusual items.

Look at margin, not just total EBITDA.

And compare cash flow too.

3. Are we ready to speak to lenders?

EBITDA can help prepare for lender conversations because lenders may use it to assess whether the business can support debt.

British Business Bank notes that banks may use EBITDA to judge business performance and assess debt repayment ability.

Before speaking to a lender, prepare:

- EBITDA

- operating cash flow

- debt repayments

- interest costs

- tax position

- cash-flow forecast

- aged debtors

- aged creditors

- working capital needs

- debt-to-EBITDA ratio

- recent management accounts

The lender is not just asking:

“Is EBITDA positive?”

They are asking:

“Can this business repay us without falling over?”

That is a different question!

4. Could the business support more borrowing?

EBITDA can help assess borrowing capacity, especially when compared with existing debt and repayment obligations.

A common measure is:

Debt-to-EBITDA ratio = Total Debt ÷ EBITDA

If total debt is £600,000 and EBITDA is £200,000:

Debt-to-EBITDA = 3.0

That means total debt is three times EBITDA.

This is not automatically good or bad.

It depends on industry, cash flow, interest rates, repayment terms, growth, and risk.

But it gives leaders a signal.

If debt is rising faster than EBITDA, risk may be increasing.

If EBITDA is rising and debt is stable, borrowing capacity may improve.

5. Are we preparing for valuation or sale?

EBITDA is often used in valuation because buyers may apply a multiple to operating earnings.

A simple valuation method is:

Estimated Enterprise Value = EBITDA × Valuation Multiple

For example:

EBITDA: £300,000

Multiple: 4x

Estimated enterprise value: £1,200,000

But do not confuse this with a guaranteed sale price.

A buyer will also look at:

- revenue quality

- customer concentration

- recurring income

- management team

- cash flow

- debt

- working capital

- growth potential

- systems

- risks

- contract quality

- market conditions

- adjusted EBITDA

British Business Bank notes that enterprise value/EBITDA is one method used in comparable business valuation.

6. Are we becoming more efficient?

EBITDA margin can show whether the business is turning revenue into operating profit more efficiently.

If revenue grows but EBITDA margin falls, the business may be getting less efficient.

That may mean:

- poor pricing

- rising wage costs

- poor job planning

- too much overtime

- inefficient routes

- weak purchasing

- too much discounting

- unprofitable customers

- poor use of equipment

- low productivity

EBITDA margin helps leaders see whether growth is healthy or just noisy.

Because not all growth is good growth.

Some growth is just a larger version of the same problem.

7. Are we comparing similar businesses?

EBITDA can help compare similar businesses, but only when the comparison is fair.

Compare within:

- the same industry

- similar business size

- similar asset needs

- similar customer types

- similar growth stage

- similar geography

- similar cost structure

- similar risk profile

Do not compare a software company with a vehicle-heavy delivery business and expect the numbers to mean the same thing.

That is like comparing a bicycle with a forklift because both have wheels!

Technically true.

Practically not helpful.

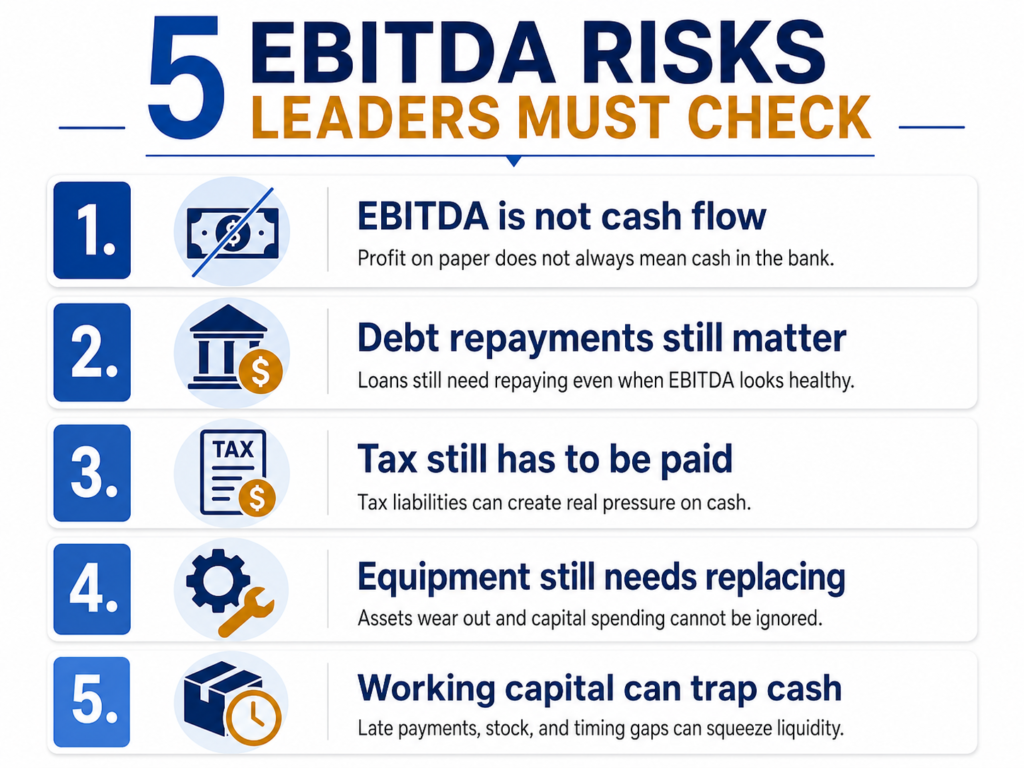

5 ways EBITDA can mislead leaders

EBITDA can mislead leaders when they treat it as cash, ignore debt repayments, forget tax, overlook equipment replacement, miss working-capital pressure, or accept over-optimistic adjustments. It is useful for operating performance, but dangerous when used as a complete picture of financial health.

Here are the five main risks:

1. EBITDA can make cash look stronger than it is

EBITDA does not show whether customers have actually paid.

A business can report strong EBITDA while cash is stuck in unpaid invoices.

That is common in service businesses, contracting, cleaning, facilities, construction, logistics, and B2B supply.

The income may be earned.

But if the money has not arrived, it cannot pay wages, tax, fuel, rent, or suppliers.

The bank does not accept “but our EBITDA is healthy” as a payment method!

Annoying, but fair.

2. EBITDA ignores debt repayments

EBITDA adds back interest, but it does not show loan repayments.

That matters because debt repayments can put real pressure on cash.

A business may have healthy EBITDA but still struggle if monthly repayments are high.

That is why leaders should also check:

- interest cover

- total debt

- repayment schedule

- debt-to-EBITDA

- cash-flow forecast

- covenant requirements

Debt is not always bad.

But misunderstood debt is dangerous.

3. EBITDA ignores equipment replacement and capital expenditure

EBITDA adds back depreciation and amortisation.

That can help comparison.

But physical assets still wear out.

Vans need replacing.

Machines need servicing.

IT systems need upgrading.

Cleaning equipment breaks.

Forklifts do not run forever, no matter how nicely you ask them.

This is why EBITDA can be misleading in asset-heavy businesses.

If the business needs regular capital expenditure, use EBITDA with capex and free cash flow.

4. EBITDA can hide working-capital pressure

Working capital means the money tied up in day-to-day operations.

This includes:

- unpaid invoices

- stock

- supplier payments

- deposits

- prepayments

- VAT timing

- payroll timing

A business may be profitable but still need more cash to fund growth.

For example:

Sales grow.

More staff are needed.

More stock is bought.

Customers take 60 days to pay.

Suppliers want payment in 30 days.

EBITDA improves.

Cash gets squeezed.

This is why fast growth can be dangerous if cash flow is not managed.

5. Adjusted EBITDA can become too optimistic

Adjusted EBITDA can be useful.

It can also become creative.

A little too creative.

Adjusted EBITDA removes unusual, one-off, or non-operating items.

That can help show normal trading performance.

But if every awkward cost is called “one-off”, the number becomes fantasy finance.

Useful adjustments may include:

- one-off legal costs

- unusual repairs

- restructuring costs

- non-recurring consultancy costs

- non-operating income

- exceptional bad debt

- owner salary adjustments

- non-market rent

But normal business costs should not be removed just because they make the number look less pretty.

Adjusted EBITDA is useful when it removes genuine one-off or non-operating items.

It becomes misleading when normal business costs are removed simply to make the business look stronger.

Before using EBITDA to support a major decision, check these five risks first:

In my experience, EBITDA becomes far more useful when leaders treat these risks as part of the decision process, not as small print to worry about later.

What is adjusted EBITDA?

Adjusted EBITDA is EBITDA after removing unusual, one-off, non-recurring, or non-operating items to show a more normal view of business performance. It is often used in valuation, lending, and investor discussions, but it should be explained clearly and supported with evidence.

Adjusted EBITDA tries to answer this question:

What would EBITDA look like in a normal trading year?

That can be useful when a business has had unusual events.

Examples include:

- one-off legal costs

- restructuring costs

- unusual repair costs

- exceptional bad debts

- non-recurring consultancy fees

- non-operating income

- one-off recruitment costs

- owner salary adjustments

- rent paid above or below market level

- unusual insurance claims

- discontinued project costs

Development Bank of Wales explains that adjusted EBITDA may remove one-time, irregular, or non-recurring items to show a clearer view of operating performance.

How leaders should use adjusted EBITDA

Use adjusted EBITDA carefully.

Ask:

- Is the adjustment genuinely unusual?

- Is it supported by evidence?

- Would a buyer or lender agree?

- Is it likely to happen again?

- Is it really non-operating?

- Are we being honest or just hopeful?

Hope is useful in leadership.

But it is not a finance policy.

How is EBITDA used in business valuation?

EBITDA is often used in business valuation by applying a valuation multiple to operating earnings. The multiple depends on industry, growth, risk, cash flow, customer quality, systems, debt, management strength, and buyer confidence. EBITDA can support valuation, but it does not decide final sale value alone.

The simple version is:

Estimated Enterprise Value = EBITDA × Valuation Multiple

For example:

EBITDA: £250,000

Multiple: 4x

Estimated enterprise value: £1,000,000

But real valuation is rarely that neat.

A buyer may reduce value if:

- customers are too concentrated

- margins are falling

- cash flow is weak

- systems are poor

- owner dependence is high

- contracts are short

- staff turnover is high

- debt is high

- equipment needs replacing

- working capital is under pressure

- growth depends on one person

A buyer may pay more if:

- revenue is recurring

- margins are strong

- cash conversion is good

- systems are reliable

- management team is strong

- customer base is diverse

- growth is believable

- risks are well managed

EBITDA is a starting point.

Not the finish line.

Why does a lender care about EBITDA?

A lender may use EBITDA to assess whether a business has enough operating profit to support debt repayments. But lenders usually also consider operating cash flow, existing debt, credit history, security, working capital, management strength, sector risk, and the quality of financial information.

If a lender asks for EBITDA, they are usually thinking about repayment capacity.

They want to know:

Can this business generate enough operating profit to support borrowing?

But they will not stop there.

They may also look at:

- management accounts

- cash-flow forecasts

- debt-to-EBITDA ratio

- interest cover

- bank statements

- aged debtors

- aged creditors

- tax arrears

- customer concentration

- existing loans

- security

- trading history

- sector risk

Useful related reading:

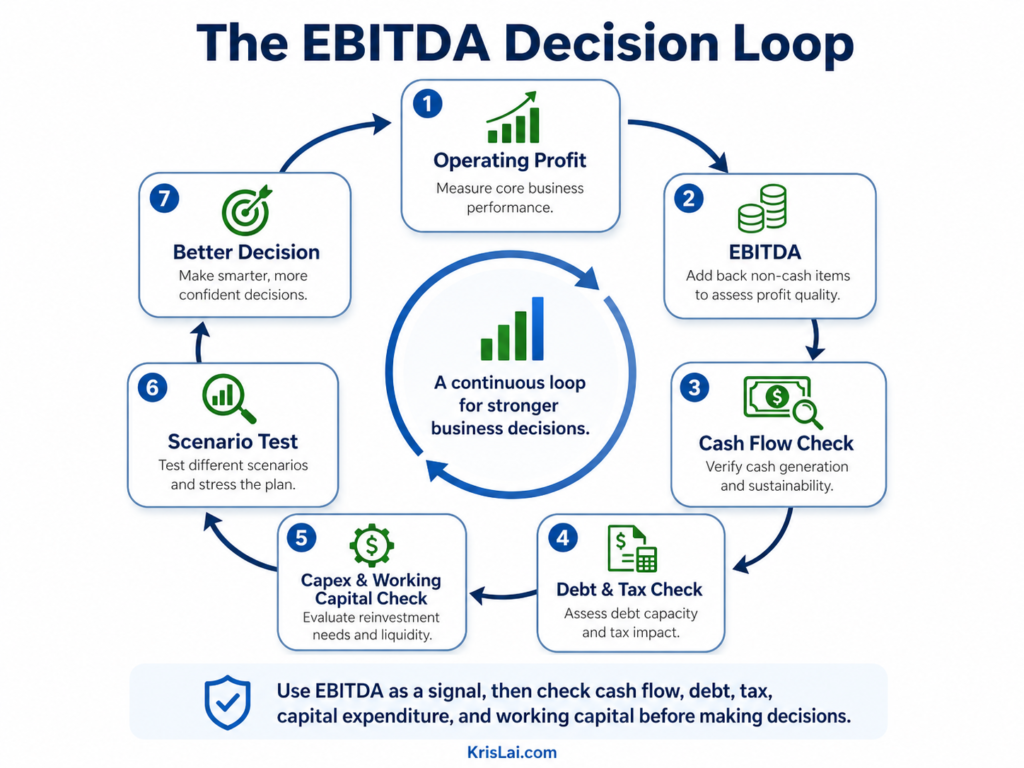

EBITDA and decision-making under uncertainty

EBITDA is more useful when leaders test it under different future scenarios instead of relying on one forecast.

This matters because business decisions are rarely made in stable conditions.

Costs move.

Interest rates change.

Customers delay decisions.

AI changes search behaviour.

Suppliers change terms.

Staff costs rise.

Technology shifts.

A single EBITDA forecast can look neat, but business life is not neat.

Use EBITDA across simple scenarios:

- base case

- slower sales

- rising costs

- delayed customer payments

- higher interest

- equipment replacement

- losing a key customer

- growth investment

- staff cost increases

This connects to practical decision methods like scenario planning, pre-mortem thinking, robust decision-making, and monitor-and-adapt reviews.

Plain English version:

Do not ask only, “What do we think will happen?”

Also ask:

“What if we are wrong?”

That one question can save a lot of money.

The KrisLai Decision Framework™ and EBITDA

A practical model for better business decisions in complex environments. It focuses on four essential elements:

- Human Behaviour — how people actually think and decide

- Signals — what people are trying to do right now

- Environment — whether the system supports good decisions

- Consequences — what happens next, and after that

Strong decisions consider all four — not just one.

EBITDA fits the KrisLai Decision Framework well.

Human Behaviour:

Are leaders using EBITDA to understand the business, or to confirm what they already want to believe?

Signals:

What is EBITDA telling us? What is it not telling us?

Environment:

What is happening around the business — interest rates, tax, customer behaviour, supplier costs, competition, sector risk, AI search changes, and finance conditions?

Consequences:

What happens if we borrow, expand, sell, invest, hire, or cut costs based on an incomplete number?

This approach is part of the KrisLai Decision Framework, a practical method for improving business decisions.

Better decisions come from understanding behaviour, signals, environment, and consequences.

This simple framework shows how I believe leaders should use EBITDA in practice: not as a final answer, but as the start of a better decision:

The key point is simple: use EBITDA as a signal, then test it against cash flow, debt, tax, capital expenditure, and working capital before acting.

What this looks like in real business

A business can have healthy EBITDA but still face pressure if debt, tax, slow-paying customers, equipment costs, or working capital are ignored. In real business, EBITDA should trigger better questions. It should not give leaders permission to expand, borrow, or sell without checking cash flow and risk.

Let’s use a practical example:

A service business has:

- revenue: £1.2 million

- EBITDA: £180,000

- EBITDA margin: 15%

- net profit: £85,000

- overdue customer invoices: £110,000

- van finance repayments: £55,000 per year

- tax due soon: £32,000

- equipment replacement needed: £40,000

- one large customer worth 35% of revenue

At first glance, EBITDA looks solid.

The business is generating operating profit.

That is good.

But cash is tight.

Why?

Customers are paying slowly.

Debt repayments are heavy.

Tax is due.

Equipment needs replacing.

Customer concentration is high.

Insight:

EBITDA says the core operation has profit potential.

Cash flow says the business is under pressure.

Decision:

Do not expand yet.

Instead:

- improve debtor collection

- review payment terms

- check pricing

- prepare a cash-flow forecast

- review finance capacity

- reduce reliance on one large customer

- plan equipment replacement

- test a slower-sales scenario

Consequence:

The business avoids a risky expansion, improves cash visibility, and enters lender conversations with stronger evidence.

That is how EBITDA should work.

Not as a green light.

As a signal that needs checking.

EBITDA can show that the business model is working, while cash flow shows whether the business can survive the timing of real payments.

Good leaders look at both.

Where this goes wrong

EBITDA goes wrong when leaders treat it as cash, use optimistic adjustments, ignore debt, forget tax, overlook equipment costs, miss working-capital pressure, or use a valuation multiple without checking business risk. The number becomes dangerous when it replaces judgement instead of supporting it.

What I’ve seen is that EBITDA often goes wrong in five common ways.

1. EBITDA becomes a comfort number

The business owner sees positive EBITDA and assumes the business is safe.

But cash may be tight.

Debt may be high.

Customers may be paying late.

Costs may be rising.

The comfort is false.

2. Adjustments become too generous

One or two genuine adjustments may be fine.

But if every cost becomes “exceptional”, the number loses credibility.

Buyers and lenders can usually smell optimistic adjustments.

And no, calling everything “strategic transformation cost” does not magically make it disappear!

3. EBITDA is used for valuation without context

A business owner hears that companies sell for “five times EBITDA”.

Then they multiply their EBITDA by five and mentally spend the money.

Dangerous.

The real multiple depends on risk, growth, cash flow, customer quality, systems, management, industry, and buyer demand.

4. Debt repayment is ignored

Interest is added back in EBITDA.

But debt still needs paying.

That repayment comes from cash.

Not from a spreadsheet cell with a nice formula in it.

5. Leaders ignore second-order consequences

A decision based on EBITDA may look good today but create pressure later.

For example:

- borrow now, struggle with repayments later

- expand now, run out of working capital later

- cut costs now, damage service quality later

- sell based on adjusted EBITDA, lose buyer trust later

- delay equipment spend, face breakdowns later

This connects closely to how I think about decisions more broadly in the KrisLai Decision Framework™.

A number is rarely just a number.

It creates behaviour.

And behaviour creates consequences.

What you should actually do

Use EBITDA as one signal, then check operating cash flow, debt payments, tax, capital expenditure, working capital, customer risk, and future scenarios before making a decision. EBITDA can support better decisions, but it should never replace judgement, cash-flow analysis, or proper business context.

Here is the practical process I would use:

Step 1: Calculate EBITDA correctly

Use one clear formula.

Then keep using the same method so trends remain comparable.

Do not change the calculation every time the number looks inconvenient.

Finance is not pick-and-mix.

Step 2: Calculate EBITDA margin

EBITDA alone can rise because the business is bigger.

EBITDA margin shows whether the business is becoming more efficient.

Use:

EBITDA margin = EBITDA ÷ Revenue × 100

Track it over time.

Step 3: Compare EBITDA with operating cash flow

Ask:

Is EBITDA rising?

Is operating cash flow also rising?

If EBITDA is strong but operating cash flow is weak, investigate:

- unpaid invoices

- stock

- supplier timing

- tax

- debt payments

- capital expenditure

- working capital

Step 4: Check debt and repayment pressure

Ask:

- What debt do we have?

- What are the repayments?

- What is the interest cost?

- What is the debt-to-EBITDA ratio?

- What happens if EBITDA falls?

- What happens if interest costs rise?

This is especially important before taking on new finance.

Step 5: Check tax and capital expenditure

EBITDA excludes tax and adds back depreciation.

But tax still needs paying.

Assets still need replacing.

Ask:

- What tax is due?

- What equipment will need replacing?

- What vehicles, systems, or machines need investment?

- What capex is required to maintain service quality?

- What capex is required for growth?

Step 6: Review working capital

Ask:

- Are customers paying on time?

- Are debtor days rising?

- Is stock increasing?

- Are suppliers being stretched?

- Are VAT or payroll timing issues creating pressure?

- Is growth consuming cash?

This is where many profitable businesses feel poor.

Step 7: Test the decision under scenarios

Before making a major decision, test EBITDA under different futures.

What happens if:

- sales fall by 10%?

- costs rise by 8%?

- a key customer leaves?

- customers pay 15 days later?

- interest costs rise?

- equipment needs replacing earlier?

- a contract is delayed?

- a new hire takes longer to become productive?

This is not pessimism.

It is leadership.

Before using EBITDA to support a major decision, ask:

- Is EBITDA rising or falling?

- Is EBITDA margin improving or weakening?

- Is operating cash flow also improving?

- Are customers paying on time?

- Are debt repayments affordable?

- Are tax bills covered?

- Do we need major equipment soon?

- Is working capital tying up cash?

- Are EBITDA adjustments reasonable?

- Are we comparing with similar businesses?

- What happens under a worse-case scenario?

EBITDA and AI search: why clear answers matter

AI tools often summarise EBITDA quickly, but summaries can miss the business risk.

That is why articles like this need direct answers, examples, tables, warnings, and decision checklists.

The future of search is changing.

Many people now ask ChatGPT, Gemini, Perplexity, Claude, or Google AI Overviews before they speak to an accountant, lender, adviser, or broker.

That means content must be useful in two ways:

- clear enough for people

- structured enough for AI tools to extract accurately

A weak article says:

“EBITDA is earnings before interest, tax, depreciation and amortisation.”

A stronger article says:

“EBITDA is useful, but do not mistake it for cash flow.”

That second answer is the one business owners actually need.

I hope this article a strong one!

Research and experience note

This article is based on practical experience, independent research, and analysis and synthesis of reliable finance sources.

Useful reference sources include:

British Business Bank: What is EBITDA?Investopedia: EBITDA definition and formula

Development Bank of Wales: Understanding EBITDA

Investopedia: Operating cash flow

I write about how better decisions are made in business — combining strategy, behaviour, and practical thinking. EBITDA is a good example of why this matters. The number helps, but the thinking around the number matters even more.

What does EBITDA actually tell you?

EBITDA tells you how much profit the core business generates before interest, tax, depreciation and amortisation. It helps show operating performance, but it does not show cash flow, debt repayments, tax payments, or capital expenditure.

Is 20% EBITDA good?

A 20% EBITDA margin may be good in some industries, but not in all. It should be compared with similar businesses, your own past performance, cash flow, debt levels, capital needs, and growth stage.

Is a 30% EBITDA margin good?

A 30% EBITDA margin can be strong, but context matters. A high margin is only useful if the business also has healthy cash flow, manageable debt, good customer quality, and enough investment for future needs.

Is EBITDA the same as gross profit?

No. Gross profit shows revenue after direct costs. EBITDA shows operating earnings before interest, tax, depreciation and amortisation. Gross profit focuses on direct margin, while EBITDA gives a broader view of operating performance.

Is EBITDA cash flow?

No. EBITDA is not cash flow. It excludes working-capital movements, debt repayments, tax payments, capital expenditure, and payment timing. A business can have strong EBITDA and still suffer cash-flow pressure.

Why is EBITDA misleading?

EBITDA can be misleading because it ignores debt repayments, tax, asset replacement, working capital, capital expenditure, and cash timing. It is useful for operating performance, but risky if treated as a complete measure of financial health.

FAQ

What is EBITDA in simple terms?

EBITDA is a measure of business profit before interest, tax, depreciation and amortisation. In simple terms, it shows how much profit the core business makes before finance costs, tax costs, and certain accounting costs are included.

How do I calculate EBITDA?

You calculate EBITDA by adding interest, tax, depreciation and amortisation back to net profit. You can also calculate it by taking operating profit and adding back depreciation and amortisation. Both methods aim to show operating earnings before those costs.

What is EBITDA margin?

EBITDA margin shows EBITDA as a percentage of revenue. It tells you how much operating profit the business keeps from each pound of sales before interest, tax, depreciation and amortisation. The formula is EBITDA divided by revenue, multiplied by 100.

What is a good EBITDA margin for a small business?

A good EBITDA margin for a small business depends on the industry, business model, size, growth stage, debt, capital needs, and cash flow. A margin that looks strong in one sector may be average in another, so compare with similar businesses.

Is EBITDA the same as net profit?

No. EBITDA is not the same as net profit. Net profit shows profit after all costs, including interest, tax, depreciation and amortisation. EBITDA adds those items back to show operating earnings before those costs are included.

Is EBITDA the same as cash flow?

No. EBITDA is not the same as cash flow. EBITDA does not include working-capital movements, debt repayments, tax payments, capital expenditure, or delayed customer payments. Operating cash flow and free cash flow give a better view of cash generation.

What is adjusted EBITDA?

Adjusted EBITDA is EBITDA after removing unusual, one-off, non-recurring, or non-operating items. It is often used in valuation, lending, and investor discussions to show a more normal view of business performance, but adjustments should be honest and evidence-based.

Why do lenders use EBITDA?

Lenders may use EBITDA to assess whether a business generates enough operating profit to support debt repayments. However, lenders also look at cash flow, existing debt, credit history, security, working capital, management strength, and sector risk.

How is EBITDA used in valuation?

EBITDA is often used in valuation by applying a multiple to operating earnings. A simple method is enterprise value equals EBITDA multiplied by a valuation multiple. The final value depends on industry, risk, growth, cash flow, systems, customers, and buyer confidence.

What should I use alongside EBITDA?

Use EBITDA alongside operating cash flow, free cash flow, debt repayments, tax, capital expenditure, working capital, EBITDA margin, customer risk, and future scenarios. EBITDA is useful, but it should not be used alone for major business decisions.

Build deeper insight

EBITDA connects closely to financial decision-making, cash flow, valuation, growth, and risk. If you want to go deeper, these articles may help:

- Small Business Budgeting: 7 Steps to Build a Smarter Budget

- Cash Flow Forecasting as an Early-Warning Decision Tool

- Financial Trend Analysis: 7 Financial Trends Leaders Should Watch

- Break-Even Analysis for Better Business Decisions

- Business Credit Score: 7 Ways to Build Borrowing Power

- Business Valuation Under Uncertainty

EBITDA is not only a finance topic. It is also a decision-making topic. These articles support the wider thinking behind better business decisions:

Conclusion and final thought: use EBITDA, but do not stop there

EBITDA is useful because it helps you see operating performance before interest, tax, depreciation and amortisation.

But it is not cash.

It is not final profit.

It is not a full valuation.

It is not a complete answer.

The real value of EBITDA comes when leaders use it as part of a wider decision process.

Over time, I’ve found that good decisions rarely come from data alone. They come from understanding people, reading signals, creating the right environment, and thinking beyond the immediate outcome.

I help people make better business decisions through psychology, strategy, and practical thinking. EBITDA is a useful example of that work: the number matters, but the thinking around the number matters more.

Run one EBITDA check this week.

Calculate EBITDA, then compare it with operating cash flow, debt repayments, tax due, capital expenditure, and working-capital pressure.

That one check will give you a clearer view of whether your business performance is genuinely strong — or just looks strong on paper.

If you want a practical way to think through business decisions, download my free KrisLai Decision Framework™ guide.

It will help you look at decisions through four simple lenses: behaviour, signals, environment, and consequences.

Use it before major choices about finance, growth, valuation, cash flow, strategy, customers, marketing, operations, and AI.

Enter your email below and I’ll send you the free KrisLai Decision Framework™ guide, a practical model for understanding behaviour, signals, environment, and consequences before problems become more expensive.

If you enjoy exploring the ideas behind better business decisions, you may find the Business Thinking Hub useful.

If you enjoy exploring the ideas behind better business decisions, you may find the Business Thinking Hub useful.

About the author

Kris Lai is a business operator and managing director with experience in land and building surveying, facilities management, logistics, and service delivery.

Earlier in his career, he worked as a Search Engine Evaluator (via Lionbridge, supporting Google), where he assessed search result relevance, user intent, and content quality using structured evaluation frameworks. This experience gives him a rare, practical understanding of how search systems interpret signals and make ranking decisions.

In parallel, whilst working with a charity organisation, he has delivered 1000’s of structured presentations in English, Finnish, and Chinese to audiences ranging from small groups to more than 600 people, and has spent decades mentoring and developing others. This experience informs his approach to clarity, communication, and decision-making under pressure.

He writes about AI, search behaviour, business strategy, and decision-making from a practical, real-world perspective.

👉 Explore ideas connected to better business decisions:

- How AI Is Changing Search Behaviour (And What Businesses Must Do Now)

- Decision-Making Framework Examples: The KrisLai Method in Action

- The KrisLai Decision Framework: A Better Way to Make Business Decisions

- Micro vs Macro Marketing: When to Target Broad Audiences vs Niche Customers

- Customer Intent Marketing: How to Turn Buying Signals Into Sales

Similar Posts

7 Financial Trends Leaders Should Watch Before Problems Grow

Financial trend analysis helps leaders spot early warning signals before problems grow. This article explains how to read revenue, margin, cash flow, debtor days, stock levels, costs, and profit quality together, so you can make better business decisions under uncertainty.

Financial Mistakes: 10 Warning Signs That Hurt Cash Flow

Financial mistakes rarely happen all at once. They begin as weak signals: tight cash flow, optimistic forecasts, rising costs, tax surprises, debt pressure, or late reports. This guide shows business leaders the 10 warning signs to watch and what to fix before small issues become expensive.

Cash Flow Forecasting for Better Decisions Under Uncertainty

Learn how cash flow forecasting helps businesses spot shortfalls early, plan with more confidence, and make better decisions under uncertainty.

Inventory Management and Cash Flow: 7 Cash-Saving Decisions

Inventory is not just stock. It is cash waiting to become useful again. This guide explains how inventory management affects cash flow, working capital, profit, stockouts, overstocking, slow-moving stock, and the decisions leaders should review before buying more stock.

How to Value a Business in Uncertain Times: 7 Valuation Traps Leaders Must Avoid

How much is your business really worth? This practical guide explains business valuation methods, common valuation mistakes, and how uncertainty, customer behaviour, leadership, and market conditions influence company value. Learn how to make better valuation decisions and avoid costly mistakes.

Business Credit Score: 7 Ways to Build Borrowing Power

Your business credit score can affect loans, supplier terms, cash flow, tenders, and growth decisions. This article explains how to check, manage, and improve your company creditworthiness before applying for finance or negotiating better payment terms.