How small businesses can understand, check, manage, and improve their company credit score before applying for finance or negotiating supplier terms.

A business credit score helps lenders, suppliers, insurers, customers, and partners judge how reliable your company is with money. Used well, it becomes more than a finance number. It becomes a decision signal for borrowing, supplier terms, cash flow, tenders, and growth timing.

A weak business credit score does not always mean your business is failing.

But it can mean other people see your business as risky.

That matters.

Because in business, perception often arrives before explanation. A lender, supplier, or potential partner may check your company before you have the chance to say, “Yes, but let me explain what happened last March…”

That explanation may be perfectly fair.

But by then, the first impression may already have been made!

This article explains:

- what a business credit score is

- why business credit scores matter

- how to check your business credit score in the UK

- what a good business credit score means

- business credit score vs personal credit score

- business credit score vs business credit report

- what affects your score

- how to improve your business credit score

- what to do before applying for finance

- how supplier terms affect cash flow

- where business owners go wrong

- how to use your score as a practical decision signa

- Your business credit score can affect loans, overdrafts, supplier terms, credit limits, insurance, tenders, and business trust.

- A business credit score is not the same as a personal credit score, although the two can overlap for small firms and newer companies.

- The score is only the summary. The business credit report shows the information behind the score.

- Payment history, debt, credit utilisation, Companies House filings, public records, CCJs, and credit applications can all affect how your business is judged.

- The best time to check your business credit score is before you need finance, not after you have been declined.

What is a business credit score?

A business credit score is a risk signal that helps lenders, suppliers, insurers, customers, and partners judge how likely a company is to pay its bills and meet financial obligations.

In simple terms, it is a way of asking:

Can this business be trusted to pay?

That may sound harsh, but that is what credit risk really means.

If a supplier gives you 30-day payment terms, they are trusting you.

If a bank offers a loan, it is trusting you.

If a finance company provides asset finance, it is trusting you.

If a customer signs a larger contract, they may want to know whether your business is stable enough to deliver.

A business credit score helps them make that judgement.

Think of your business credit score like a reputation score for how your company handles money.

It does not tell the full story of your business. It does not know how hard you work, how loyal your customers are, or how many late nights you have spent fixing problems. But it gives outsiders a quick signal about payment behaviour, credit risk, and financial reliability.

That is why it matters. It shapes how other businesses may judge you before they speak to you.

What is a business credit score? The direct answer:

A business credit score summarises how creditworthy your company looks based on information such as payment history, debt, credit applications, company records, public filings, CCJs, and other financial behaviour.

The score may be used by:

- banks

- alternative lenders

- suppliers

- insurers

- landlords

- customers

- business partners

- credit reference agencies

- trade credit providers

It is not just about borrowing.

It can affect how much trust other organisations place in your business.

Useful reference sources:

Lloyds Bank: Understanding your business credit scoreBritish Business Bank: Business credit scores and finance options

Experian: What is a business credit score?

Xero: What is a business credit score?

Idea Bridge: from finance number to decision signal

Many business owners only think about their business credit score when they need money.

That is understandable.

It is also risky.

By the time you are applying for a loan, overdraft, asset finance, or supplier credit, the score may already be affecting your options.

So the better way to think about it is this:

Your business credit score is not just a finance number.

It is a decision signal.

It helps you decide:

- when to apply for finance

- whether to improve your position first

- which supplier terms to negotiate

- whether the business looks stable enough for bigger contracts

- whether cash flow pressure is starting to show

- whether your financial habits support growth

- whether other businesses may see you as high or low risk

In my experience, small businesses often pay attention to credit scores after a problem appears.

But the smarter move is to check the signal earlier.

As the Swedish saying goes: “Bättre förekomma än förekommas.”

It means, roughly, “Better to prevent than to be prevented.”

That is very true with business credit.

It is much easier to prepare before a finance application than to explain a poor score after rejection.

Why does your business credit score matter?

Your business credit score matters because it can affect whether you get finance, what interest rate you pay, what credit limit you receive, whether suppliers offer payment terms, and whether other companies see you as reliable.

It can affect:

- business loans

- overdrafts

- asset finance

- invoice finance

- supplier credit terms

- trade credit

- credit limits

- insurance decisions

- lease agreements

- tenders

- major customer contracts

- growth timing

- cash-flow flexibility

This is why business credit scores matter for real-world business decisions.

A stronger score may improve your borrowing power.

A weaker score may mean more questions, higher costs, lower limits, fewer options, or a declined application.

That does not mean a score is the only thing that matters.

Lenders and suppliers may also look at revenue, trading history, bank statements, accounts, cash flow, directors, sector risk, and the purpose of the finance.

But the score often helps shape the first impression.

Your business credit score does not only affect whether you can borrow. It can affect when you can act.

A stronger credit position gives a business more choice. More choice usually means better decisions.

Does my Ltd company have a credit score?

Yes, a limited company can have its own business credit score, although lenders may still consider director or owner credit history, especially if the company is new or has little trading history.

This is an important point.

A limited company is legally separate from you as an individual.

That means the company can build its own credit profile.

However, for small businesses, startups, and companies with limited trading history, lenders may still look at the owner or director’s personal credit position. They may also ask for a personal guarantee.

So, while business credit and personal credit are different, they may still connect in real life.

Especially when the business is young.

Especially when the business has little credit history.

Especially when the finance provider wants extra comfort.

That is not always pleasant.

But it is practical reality.

Can a business have a credit score?

Yes, a business can have a credit score if credit reference agencies and reporting services have enough information to assess the company’s creditworthiness.

A limited company may build a score through:

- company registration

- filed accounts

- payment history

- supplier accounts

- credit agreements

- public records

- finance applications

- director information

- trading history

- business banking behaviour

A sole trader is different because the business and the individual are not legally separate in the same way. In that case, personal credit may play a much larger role.

Business credit score vs personal credit score

A business credit score measures the creditworthiness of a company; a personal credit score measures the creditworthiness of an individual.

Both matter, but they are not the same.

| Business Credit Score | Personal Credit Score |

|---|---|

| Linked to the company or business | Linked to the individual |

| Used by lenders, suppliers, insurers, customers, and partners | Used for personal borrowing, mortgages, credit cards, and some business finance checks |

| Based on company payment behaviour, filings, public records, debts, and credit activity | Based on personal borrowing, repayment history, credit use, electoral roll, and other individual data |

| More relevant for limited companies with trading history | More relevant for sole traders, new businesses, and personal guarantees |

The decision point is this:

Do not assume your business credit score protects you from personal credit checks.

And do not assume your personal credit score automatically builds a strong company credit profile.

For many small businesses, both need attention.

Business credit score vs business credit report

A business credit score is the summary number; a business credit report shows the information behind that number.

This matters because a score on its own can be misleading.

A business credit report may include:

- company name and address

- registration details

- directors

- shareholders or ownership details

- filed accounts

- payment history

- credit limits

- credit searches

- public records

- CCJs

- insolvency information

- recommended credit limit

- risk indicators

The score tells you the result.

The report tells you the story.

And the story is where the useful decisions sit.

A business credit score is a quick summary of risk. A business credit report shows the details behind that risk, such as payment history, company filings, debts, public records, credit searches, and possible warning signs.

What is a good business credit score?

A good business credit score depends on the credit reference agency, but in the UK, higher scores usually mean lower risk and stronger creditworthiness.

This is where many business owners get confused.

There is no single universal score used by every provider.

Different credit reference agencies may use different ranges and methods.

Some business scores use a 0 to 100 scale.

Others may use different scoring models.

So, instead of obsessing over one number, look at:

- whether your score is improving or falling

- whether you are seen as low risk

- what the report says is affecting the score

- whether lenders or suppliers ask for more information

- whether the score supports your next business decision

As a general rule, on some UK business credit scoring models, a higher score suggests lower risk. Some UK guides refer to scores above 80 as strong or excellent on a 0 to 100 scale.

But always check which agency and scoring model is being used.

A score without context is like a weather forecast without a location.

It may sound useful, but you still do not know whether to bring an umbrella!

How do you check your business credit score in the UK?

You can check your business credit score through UK credit reference agencies and business credit platforms such as Experian, Equifax, Dun & Bradstreet, Creditsafe, Capitalise, and other commercial reporting services.

Some checks are free.

Some are paid.

Some give a simple summary.

Some give a more detailed business credit report.

A good approach is to check at least one recognised provider before you need finance.

If the decision is important, check more than one.

Why?

Because different providers may hold different information or present risk differently.

When checking your score, you may need:

- your company name

- company registration number

- registered address

- trading address

- director details

- basic business information

Look for:

- wrong company details

- old addresses

- incorrect director information

- late payment records

- unexpected credit searches

- CCJs

- filing issues

- debt pressure signals

- mismatched information

Check your business credit score before you need finance. Waiting until after a declined application is like checking the fuel gauge after the car has stopped.

What affects your business credit score?

Your business credit score can be affected by payment history, debt levels, credit utilisation, credit applications, public records, CCJs, Companies House filings, business age, financial stability, and whether your company details are accurate.

Here is the practical version:

| Factor | Why It Matters | Better Decision |

|---|---|---|

| Payment history | Shows whether the business pays reliably | Pay before the due date where possible |

| Debt levels | High debt may suggest financial pressure | Avoid borrowing more than the business can comfortably service |

| Credit utilisation | Using too much available credit can look risky | Keep headroom where possible |

| Credit applications | Too many applications may suggest stress | Apply selectively and prepare first |

| CCJs and public records | Can raise serious risk concerns | Resolve problems quickly and keep records clean |

| Companies House filings | Late or unclear filings reduce trust | File accounts and confirmation statements on time |

| Supplier payment data | Shows how the business behaves with trade credit | Use supplier credit responsibly and pay agreed terms |

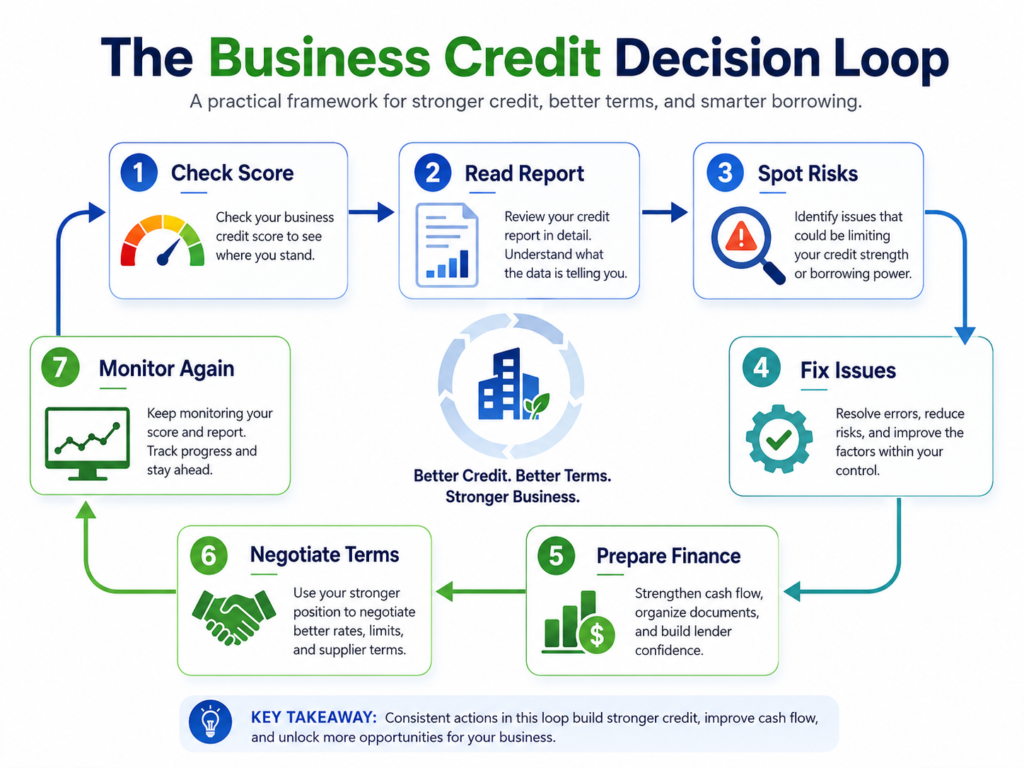

The simplest way to think about business credit is as a practical decision loop, not a one-off number.

In my experience, business credit becomes much more useful when you treat it as an ongoing process of checking, fixing, preparing, and reviewing rather than something you only think about when a lender says no.

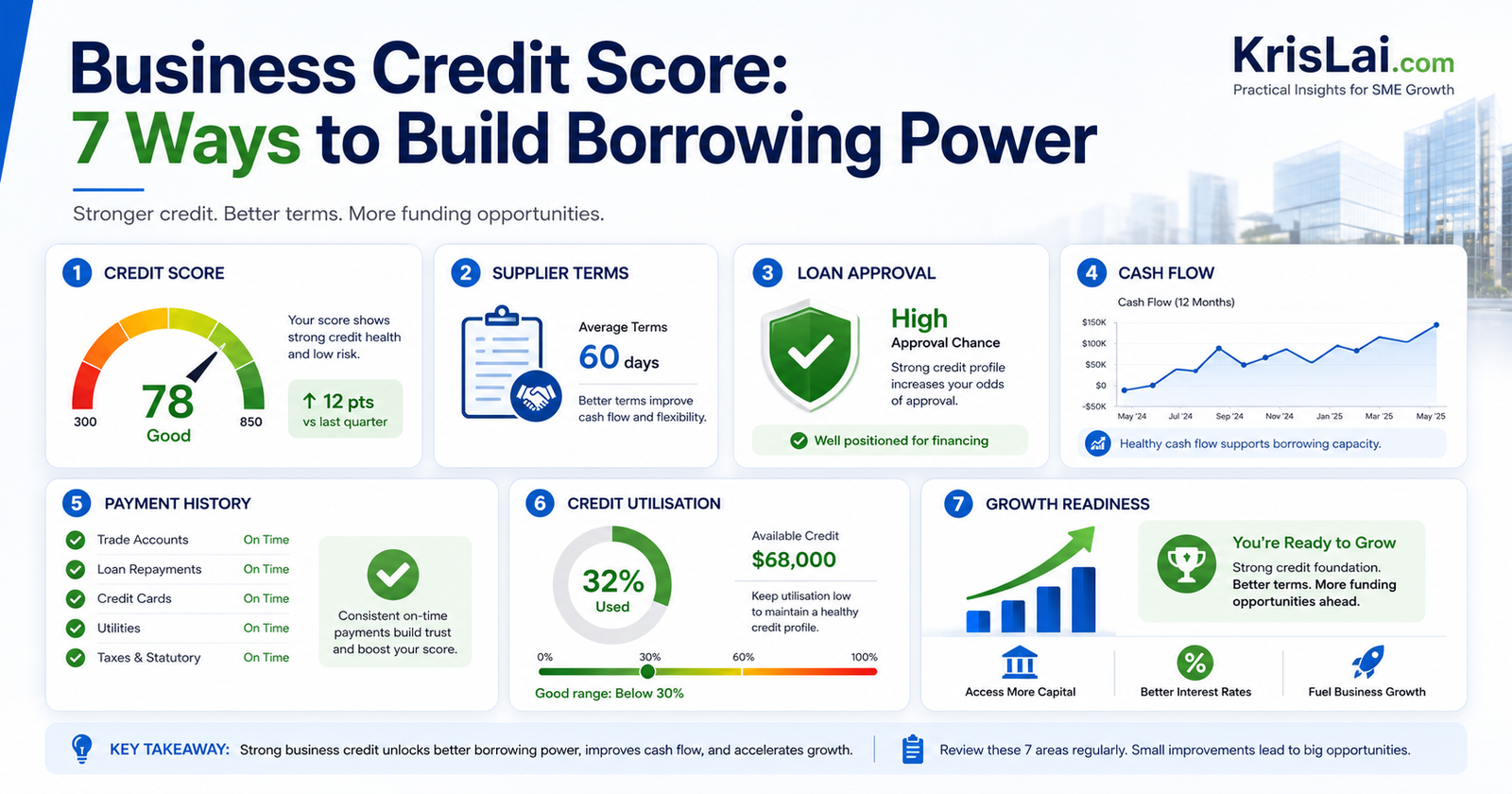

7 ways to build borrowing power

To improve your business credit score, check your report, pay on time, control credit use, separate finances, file company information properly, use supplier credit carefully, and apply for finance selectively.

Let’s go through those steps.

1. Check your business credit report before you need finance

You get your business credit score by checking your company profile with a credit reference agency or business credit platform.

Do this before you apply for a loan, overdraft, asset finance, or supplier credit.

The report may show errors or weak spots you can fix.

For example:

- wrong address

- missing company information

- old director details

- late filing issue

- unexpected search

- disputed invoice

- old payment issue

- CCJ you need to deal with

- weak trading history

- high suggested risk

What I’ve seen in business is that people often manage what they can see.

If you do not check the report, you are guessing.

And guessing is not a great financial strategy.

It is very popular, unfortunately.

But still not great.

2. Pay bills, suppliers, and finance agreements on time

Paying on time is one of the strongest ways to protect and improve your business credit score.

This includes:

- supplier invoices

- business loans

- leases

- credit cards

- utilities

- tax payment arrangements

- asset finance

- trade credit accounts

Late payments create doubt.

Repeated late payments create a pattern.

A pattern creates a risk signal.

If cash flow is tight, speak to suppliers early.

Most suppliers would rather hear from you before the payment is late than chase you afterwards.

Silence rarely builds trust.

It usually builds suspicion.

3. Keep credit utilisation under control

Credit utilisation means how much of your available credit you are using.

If the business is constantly close to its limit, it may look stretched.

This can apply to:

- business credit cards

- overdrafts

- trade credit

- credit accounts

- revolving finance

A business that uses 95% of every available facility may still be paying on time.

But it may also look as if there is little breathing room.

Credit scores are often about signals.

High utilisation can signal pressure.

The better decision is to keep some headroom where possible.

That gives your business more flexibility.

It also gives you more room if customers pay late or costs rise.

Useful related reading:

Cash Flow Forecasting as an Early-Warning Decision Tool4. Keep personal and business finances separate

Separate finances make your business look more organised and help build a clearer company credit profile.

For a limited company, this usually means:

- using a business bank account

- keeping business expenses separate

- avoiding personal spending through business accounts

- using business credit facilities for business needs

- keeping clear records

- paying yourself properly

- working with your accountant when needed

This does not mean personal credit never matters.

For small businesses, personal guarantees and director checks can still appear in finance decisions.

But separating finances helps make the business easier to understand.

And an easier-to-understand business is often easier to trust.

5. File accounts and company information on time

Late or unclear company information can damage trust and make lenders or suppliers more cautious.

For limited companies, Companies House information matters.

Keep up to date:

- annual accounts

- confirmation statement

- registered office

- directors

- persons with significant control

- SIC code

- company name and address

- filing deadlines

A business that files late may be perfectly honest.

But from the outside, late filing can look like poor control.

Or worse, financial stress.

Again, this is about signals.

One late filing may not tell the whole story.

But it can still create doubt.

And doubt is expensive.

6. Use supplier trade credit carefully

Supplier credit terms can help cash flow and build a useful payment history if you pay reliably.

For example, 30-day supplier terms can help you buy stock, materials, or services before customer money comes in.

That can support working capital.

But supplier credit is not free money.

It is trust with a due date.

Use it well and it can help your business credit profile.

Use it badly and it can damage supplier relationships and creditworthiness.

Ask yourself:

Can we pay this supplier on time?

Is this helping cash flow or hiding a cash-flow problem?

Do we know when the payment is due?

Would late payment damage a key relationship?

Can supplier terms help us avoid more expensive borrowing?

Supplier terms are not just admin.

They are a cash-flow decision.

Useful related reading:

Financial Dashboards That Help Leaders Make Better Decisions7. Apply for credit selectively

Too many credit applications in a short period can make a business look under pressure.

Before applying, prepare.

Check:

- why you need the finance

- how much you need

- whether the amount is realistic

- whether you can repay comfortably

- what documents are required

- whether your credit report has errors

- whether your cash flow supports the application

- whether a softer quote or eligibility check is available

- whether supplier terms could be a better option

Panic applications are dangerous.

They often happen when the business is already under pressure.

That is exactly when a lender may be more cautious.

A better approach is to prepare before the pressure peaks.

What should you do before applying for business finance?

Before applying for business finance, check your credit report, correct errors, prepare accounts, understand cash flow, reduce avoidable debt, avoid unnecessary applications, and decide how the finance will improve the business.

This is where the business credit score becomes a decision tool.

Before you apply, ask:

What problem will this finance solve?

Will it improve revenue, margin, cash flow, capacity, or resilience?

Can the business repay it without creating stress?

What happens if sales are slower than expected?

What happens if costs rise?

What happens if customers pay late?

What would make this finance decision fail?

That last question is important.

It is a simple pre-mortem.

You imagine the decision went wrong and ask why.

This can reveal risks before you sign anything.

- Check your business credit report.

- Correct errors or old information.

- Review payment history.

- Check your cash-flow forecast.

- Review credit utilisation and debt levels.

- Prepare accounts, bank statements, and management figures.

- Decide exactly what the finance will achieve.

- Avoid multiple rushed applications.

- Know your comfortable repayment level.

Useful related reading:

How supplier terms can improve cash flow

Good supplier terms can improve cash flow by giving your business more time to pay, but they only help if the business manages payment dates carefully.

Supplier terms can support cash flow because they affect timing.

If you receive money from customers after you pay suppliers, cash flow tightens.

If you receive money before paying suppliers, cash flow becomes easier.

That timing gap matters.

Supplier terms can help bridge the gap.

But only if the business uses them responsibly.

A 30-day payment term is useful.

A 30-day payment term that quietly becomes 60 days because nobody is watching the calendar is a problem.

That may damage supplier trust.

It may damage your business credit profile.

It may also make a key supplier less willing to support you when you need help.

Supplier relationships are part of financial resilience.

Treat them that way.

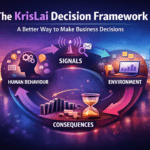

The KrisLai Decision Framework™ and business credit scores

A practical model for better business decisions in complex environments. It focuses on four essential elements:

- Human Behaviour — how people actually think and decide

- Signals — what people are trying to do right now

- Environment — whether the system supports good decisions

- Consequences — what happens next, and after that

Strong decisions consider all four — not just one.

Business credit scores fit the KrisLai Decision Framework very well.

Human behaviour:

People often delay checking their credit score because it feels dull, scary, or easy to ignore.

Signals:

Late payments, rising debt, high utilisation, credit searches, filing delays, and supplier pressure all send signals.

Environment:

Cash flow, customer payment behaviour, supplier terms, interest rates, lender caution, and market pressure shape decisions.

Consequences:

A weak score can affect borrowing, supplier terms, tenders, credit limits, and growth timing.

This approach is part of the KrisLai Decision Framework, a practical method for improving business decisions.

Better decisions always come from understanding behaviour, signals, environment, and consequences.

Business credit score and decision-making under uncertainty

Your business credit score is a signal, not the whole story.

That is important.

A score can help guide decisions, but it should not replace judgement.

For example, imagine you are considering finance for new equipment.

You could:

- apply now

- wait 90 days

- reduce credit use first

- correct report errors first

- improve supplier payment habits

- use supplier terms instead

- delay the purchase

- lease instead of buy

- run a smaller trial first

Those are decision options.

A strong decision compares them.

In decision-quality terms, good decisions need the right frame, useful information, real alternatives, clear trade-offs, sound reasoning, and commitment to action.

That is why your business credit score should be reviewed alongside:

- cash-flow forecast

- profit margin

- customer demand

- current debt

- payment habits

- supplier relationships

- timing

- risk

- consequences

Over time, I’ve found that good decisions rarely come from data alone. They come from understanding people, reading signals, creating the right environment, and thinking beyond the immediate outcome.

That is true in finance as well.

Useful reference:

Strategic Decisions Group: Decision QualityWhat this looks like in real business

Imagine a small cleaning or facilities business.

The owner wants to buy new equipment, take on a larger contract, and negotiate better supplier terms.

On paper, the opportunity looks good.

More work.

Better customer.

Bigger contract.

Growth.

Lovely.

But then the business credit report shows a few problems.

There were late supplier payments last year.

The business credit card is often near its limit.

The company filed accounts close to the deadline.

There have been several finance searches in a short period.

None of this means the business is doomed.

It means the business may look riskier than the owner expected.

Insight:

The issue is not only the score.

The issue is decision readiness.

Real example:

The owner wants to apply for finance immediately. But the report shows signs that could weaken the application.

Decision:

Instead of rushing, the owner checks the report, corrects a wrong address, sets payment reminders, reduces card usage, speaks to two suppliers about clearer payment terms, and waits 90 days before applying.

Consequence:

The business applies from a stronger position.

It has better documents, clearer cash flow, fewer avoidable concerns, and more confidence in the decision.

That is the point!

The score is not just a number.

It helps the business decide when to move, when to wait, and what to fix first.

A business credit score is most useful before a major decision. Check it before finance, tenders, supplier negotiations, large purchases, and growth moves.

Where this goes wrong

Business credit score management goes wrong when owners only check after rejection, mix personal and business finances, pay late, use too much credit, ignore public records, apply too often, or treat supplier terms as free money.

Here are the common mistakes:

Only checking after a finance rejection

This is very common.

But by then, the decision window may already be closing.

Check earlier.

Mixing personal and business finances

This makes the business harder to understand and can weaken the company’s credit profile.

Clean records matter.

Paying late

Late payments damage trust.

Repeated late payments create a pattern.

Patterns matter.

Using too much available credit

High utilisation can make the business look stretched, even if payments are still being made.

Applying for too much credit too quickly

Too many applications may make the business look desperate.

That may be unfair.

But credit decisions often rely on signals.

Ignoring CCJs or public records

A CCJ can be a serious warning sign.

Deal with issues quickly and get proper advice where needed.

Filing accounts late

Late filing can look like poor control.

It can also damage trust with lenders and suppliers.

Assuming all scores are the same

Different agencies may use different models.

Check the report, not just the number!

The worst time to discover a weak business credit score is when you urgently need finance.

Check the signal before the decision becomes urgent.

Can I get a business loan with a bad credit score?

You may be able to get a business loan with a bad credit score, but your options may be more limited, more expensive, or require extra security, a personal guarantee, or stronger supporting evidence.

A poor score does not always mean “no”.

But it can mean:

- fewer lenders

- higher interest rates

- lower credit limits

- more questions

- more documents

- shorter terms

- security requirements

- personal guarantee requests

- declined applications

This is why preparation matters.

Before applying, ask:

Is the score weak because of old issues?

Are there errors?

Can we improve the position first?

Can we show strong cash flow?

Can we explain the purpose clearly?

Can we reduce risk for the lender?

Can we wait and apply from a stronger position?

A “bad credit” loan may sometimes be necessary.

But do not rush into expensive finance just because it is available.

Available does not always mean wise.

How long does it take to improve a business credit score?

Improving a business credit score usually takes consistent action over time, because credit reference agencies need updated payment, filing, and financial behaviour before the score changes.

Some changes may show faster.

For example:

- correcting wrong data

- filing overdue information

- resolving errors

- reducing high utilisation

Other improvements take longer.

For example:

- building payment history

- reducing debt

- improving trading stability

- building supplier trust

- showing consistent financial behaviour

The practical answer is:

Do the right things early.

Then keep doing them.

Creditworthiness is built through patterns.

Not promises.

Can suppliers check my business credit score?

Yes, suppliers may check your business credit score or credit report before offering trade credit, payment terms, or higher credit limits.

This is especially likely if:

- you want 30-day or 60-day terms

- you are a new customer

- the order value is large

- the supplier has never traded with you

- your sector is seen as higher risk

- you ask for a higher credit limit

This is why business credit score management is not only about banks.

It is also about trust across your supply chain.

Can AI help with business credit score management?

AI can help business owners monitor patterns, summarise finance data, spot late-payment risks, draft supplier messages, and forecast cash-flow pressure, but it cannot fix poor financial habits.

AI can support:

- cash-flow forecasting

- invoice reminders

- payment-risk alerts

- supplier communication drafts

- management report summaries

- finance application preparation

- scenario planning

- customer payment trend analysis

- credit-control workflows

But AI cannot make late payments disappear.

It cannot replace proper accounting.

It cannot guarantee finance approval.

It should not replace professional financial advice.

AI is useful when it helps you notice signals earlier.

It is dangerous when it gives false confidence.

This also connects to changing search behaviour.

People increasingly use AI tools to ask business finance questions before speaking to a bank, accountant, or advisor. That means useful, practical, trustworthy content matters more than ever.

If your business provides financial, advisory, or professional services, the same principle applies to your customers.

They are searching differently.

They are comparing earlier.

They are forming views before they contact you.

Useful related reading:

How AI Is Changing Search BehaviourHow do I get my business credit score?

You can get your business credit score by checking your company with a recognised business credit reference agency or commercial credit reporting platform.

Does my Ltd company have a credit score?

Yes, a limited company can have its own business credit score, although lenders may still consider director credit history if the company is new or has limited trading history.

What is a good credit score for a small business?

A good score depends on the agency used, but higher scores usually mean lower risk. On some UK 0 to 100 scoring systems, scores above 80 are often seen as strong.

Can I check another company’s credit score?

Yes, many business credit reporting services allow you to check another company’s credit report, which can help when assessing customers, suppliers, or partners.

Does my personal credit score affect my business credit?

It can, especially for sole traders, new businesses, director checks, and finance applications involving a personal guarantee.

What you should actually do

Start with this one thing:

Check your business credit report before you need finance.

That is the simplest useful action.

Then do this:

- Check your score with at least one recognised provider.

- Read the report, not just the number.

- Look for errors or outdated information.

- Check Companies House details.

- Review payment history.

- Set up reminders for key bills.

- Keep credit utilisation under control.

- Avoid rushed credit applications.

- Speak to suppliers early if cash flow is tight.

- Review the score again before a major finance decision.

This connects closely to how I think about decisions more broadly in the KrisLai Decision Framework™.

A business credit score should not create panic.

It should create clarity.

It tells you what others may see.

Then you can decide what to fix first.

If you want to simplify business credit score management, these are the seven decisions worth reviewing again and again:

In my experience, business credit becomes much easier to manage when you stop treating it as a mystery number and start treating it as a set of practical decisions.

Before your next finance application, supplier negotiation, tender, or large purchase, check your business credit report and write down the top three issues that could weaken trust.

Then fix what you can before the decision becomes urgent.

FAQ

What is a business credit score?

A business credit score is a risk signal that helps lenders, suppliers, insurers, customers, and partners judge how likely a company is to pay bills and meet financial obligations.

How do I check my business credit score?

You can check your business credit score through a recognised credit reference agency or business credit reporting platform. In the UK, providers may include Experian, Equifax, Dun & Bradstreet, Creditsafe, Capitalise, and other commercial services.

Does my Ltd company have a credit score?

Yes, a limited company can have its own business credit score. However, lenders may still consider director or owner credit history, especially if the business is new or has limited trading history.

Can a business have a credit score?

Yes, a business can have a credit score if enough information exists for credit reference agencies to assess its creditworthiness. This may include company filings, payment history, debt levels, credit searches, and public records.

What is a good business credit score for a small business?

A good business credit score depends on the agency and scoring model used. In general, higher scores suggest lower risk. On some UK 0 to 100 models, scores above 80 are often considered strong.

Is a business credit score different from a personal credit score?

Yes. A business credit score measures company creditworthiness, while a personal credit score measures individual creditworthiness. However, personal credit may still matter for sole traders, new businesses, director checks, and personal guarantees.

What affects a business credit score?

A business credit score may be affected by payment history, debt levels, credit utilisation, credit applications, Companies House filings, public records, CCJs, trading history, financial stability, and accuracy of company information.

How do I improve my business credit score?

You can improve your business credit score by paying bills on time, checking your report, correcting errors, filing company information on time, keeping credit utilisation under control, reducing avoidable debt, using supplier terms responsibly, and applying for credit selectively.

Can I get a business loan with a bad credit score?

You may be able to get a business loan with a bad credit score, but options may be more limited or expensive. Lenders may ask for more evidence, security, a personal guarantee, or stronger cash-flow information.

How long does it take to improve a business credit score?

It can take time to improve a business credit score because agencies need updated evidence of better payment, filing, and financial behaviour. Some corrections may show sooner, but long-term improvement usually comes from consistent good habits.

Can suppliers check my business credit score?

Yes. Suppliers may check your business credit score before offering trade credit, payment terms, or higher credit limits. This is especially common for new customers or larger orders.

Should I check another company’s credit score?

Yes, checking another company’s credit score can be useful before offering payment terms, accepting a large order, entering a partnership, or relying on a key supplier.

Research and experience note

This article is based on practical experience, independent research, and analysis of how business credit scores affect small and medium-sized business decisions.

Useful reference sources include:

British Business Bank: Nine ways to improve your business credit scoreBritish Business Bank: Business credit score and finance optionsLloyds Bank: Understanding your business credit score

Experian: What is a business credit score?

Iwoca: How to check your business credit score

Capitalise: What is a good business credit score?

Xero: What is a business credit score?

Strategic Decisions Group: Decision Quality

The aim is not to turn credit scores into a fear exercise.

The aim is to help business owners see the signal earlier, make better decisions, and protect borrowing power before it is needed.

Business credit scores are not only a finance topic. They connect to behaviour, customer trust, cash flow, risk, and second-order consequences.

These articles may help you go deeper:

Useful related reading:

Conclusion and final thoughts

If you remember nothing else, remember this:

Check your business credit report before you need finance.

That one habit gives you time.

Time to correct errors.

Time to improve payment habits.

Time to reduce avoidable pressure.

Time to prepare better documents.

Time to decide whether to apply now, wait, negotiate, or choose another route.

A business credit score is not the whole business.

But it can affect how others judge the business.

I help people make better business decisions through psychology, strategy, and practical thinking. In this case, better thinking means treating your business credit score as an early signal, not an afterthought.

Free Guide: Better Business Decisions Under Pressure

Financial pressure rarely begins with one dramatic event. It usually starts with small signals that are easy to miss.

Enter your email below and I’ll send you the free KrisLai Decision Framework™ guide, a practical model for understanding behaviour, signals, environment, and consequences before problems become more expensive.

It is designed to help leaders think more clearly and act earlier when timing, pressure, and uncertainty begin to build.

If you enjoy exploring the ideas behind better business decisions, you may find the Business Thinking Hub useful.

About the author

Kris Lai is a business operator and managing director with experience in land and building surveying, facilities management, logistics, and service delivery.

Earlier in his career, he worked as a Search Engine Evaluator (via Lionbridge, supporting Google), where he assessed search result relevance, user intent, and content quality using structured evaluation frameworks. This experience gives him a rare, practical understanding of how search systems interpret signals and make ranking decisions.

In parallel, whilst working with a charity organisation, he has delivered 1000’s of structured presentations in English, Finnish, and Chinese to audiences ranging from small groups to more than 600 people, and has spent decades mentoring and developing others. This experience informs his approach to clarity, communication, and decision-making under pressure.

He writes about AI, search behaviour, business strategy, and decision-making from a practical, real-world perspective.

👉 Explore ideas connected to better business decisions:

- How AI Is Changing Search Behaviour (And What Businesses Must Do Now)

- Decision-Making Framework Examples: The KrisLai Method in Action

- The KrisLai Decision Framework: A Better Way to Make Business Decisions

- Micro vs Macro Marketing: When to Target Broad Audiences vs Niche Customers

- Customer Intent Marketing: How to Turn Buying Signals Into Sales

Similar Posts

Problem-Solving in Business: How to Find the Real Issue, Make Better Decisions, and Fix What Matters

Master problem-solving in business with effective strategies and real-life examples. Learn key techniques, overcome obstacles, and foster a problem-solving mindset in your team to drive success and innovation. Read more on Krislai.com!

Data-Driven Marketing: How Logic, Proof, and Clear Decisions Improve Results

Learn how data-driven marketing uses logic, proof, structure, and evidence to improve trust, reduce friction, and strengthen marketing decisions and conversions.

- Strategy & Business Thinking | Behavioural Economics & Decision Psychology | Marketing & Customer Behaviour

Micro-Moment Marketing: How Small Moments Drive Big Buying Decisions

Micro-moment marketing helps you reach customers exactly when they’re ready to act. Learn the strategy, examples, and practical steps to win these moments.

Business Development Manager: The Key to Unlocking Growth Opportunities

Discover the role of a business development manager. Learn about responsibilities, essential skills, tools, and tips for excelling in this dynamic, growth-focused role.

Innovation Under Pressure: How Leaders Decide What to Change and What to Keep

Learn how leaders handle innovation under pressure by deciding what to change, what to keep, and what to test before making bigger moves.