Cash problems rarely arrive with a polite warning.

More often, they creep in quietly.

Sales look fine. Profit looks acceptable. The business seems busy enough. Then a few large bills land, a customer pays late, VAT is due, and suddenly the pressure is very real.

That is why cash flow forecasting matters.

A cash flow forecast helps you estimate when money is likely to come in, when it is likely to go out, and whether the timing between the two could create trouble. In simple terms, it helps you see whether your business is likely to have enough cash to cover what is coming. Cash flow projections are part of the same practical process. They help you look ahead rather than guess under pressure.

In my experience, the real value is not just financial tidiness. It is better judgement.

A good forecast helps you spot problems earlier, stay calmer, and make better decisions when sales, costs, and payment timing are uncertain. It helps you decide whether you can afford to hire, buy stock, delay spending, push harder on debt collection, or speak to a lender before the problem becomes urgent.

This is one reason I see cash flow forecasting as more than a finance exercise. It is a decision tool.

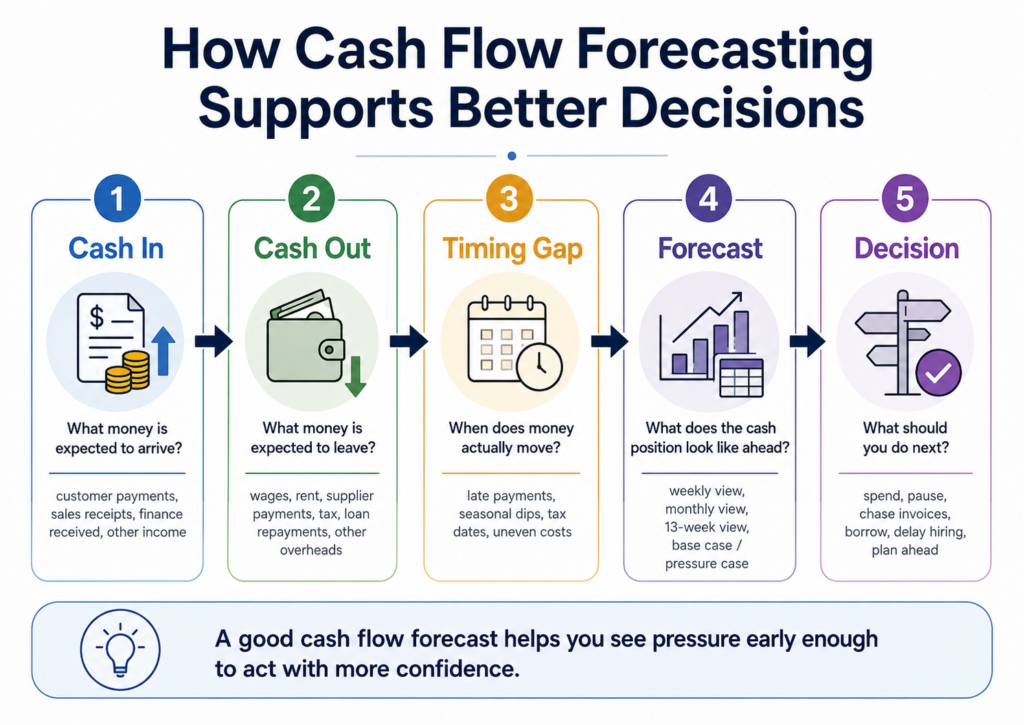

This approach is part of the KrisLai Decision Framework, a practical method for improving business decisions. Better decisions come from understanding behaviour, signals, environment, and consequences. Cash flow forecasting fits that perfectly. It gives you signals before a cash problem becomes a crisis.

Cash flow forecasting helps you see whether cash will arrive in time to cover what the business needs to pay. It is not just about predicting numbers. It is about spotting pressure early enough to make better decisions.

Key takeaways

- Profit is not the same as cash

- Timing matters more than many business owners expect

- A forecast is most useful when it is realistic, updated often, and used to guide action

- Late payments, tax bills, and uneven trading can quickly distort a hopeful forecast

- The best cash flow forecasts act as early-warning systems, not just finance documents

What does cash flow forecasting actually tell you?

Cash flow forecasting tells you whether the business is likely to have enough money available, at the right time, to meet its obligations.

That sounds simple, but it matters a great deal.

A business can look healthy on paper and still come under cash pressure. That is because profit and cash are not the same thing. A sale may count as revenue now, but the cash might not arrive for 30, 60, or even 90 days. Meanwhile, wages, rent, suppliers, and tax do not usually wait with much sympathy.

This is one reason the stronger cash flow guides put so much emphasis on timing rather than just totals. Xero’s guide to cash flow forecasting is particularly clear on this, and the British Business Bank guide also frames forecasting around the movement of cash through the business rather than simple paper performance.

Why can profit look fine while cash still runs short?

Because accounting profit and available cash move on different clocks.

Imagine this:

You invoice a customer for £20,000 in March. On paper, that may help your profit. But if the customer does not pay until May, the cash is not available in March when payroll, suppliers, rent, VAT, and loan payments are due.

So yes, the business may be profitable.

It may also be short of money.

What I have seen is that this catches good businesses out more often than they expect. Not because they are careless, but because profit feels reassuring while cash timing is much less polite.

That is why forecasting matters. It forces you to deal with reality as it moves, not just as it looks in a report.

How do cash flow projections help with day-to-day planning?

A forecast supports practical decisions such as:

- whether you can afford to hire

- whether you should delay a purchase

- whether to buy stock now or later

- whether you need to chase overdue invoices more firmly

- whether to slow spending

- whether to ask for finance before the gap becomes painful

This is where cash flow forecasting becomes more useful than many people realise. It is not just a spreadsheet for accountants. It is a way to reduce guesswork.

If you are also working on broader financial visibility, this connects well with your dashboard thinking in Financial Dashboards That Help Leaders Make Better Decisions and your work on 5 Financial Ratios Every Business Leader Should Understand.

A cash flow forecast does not just tell you what might happen. It helps you decide what to do next. That is why it belongs in leadership thinking, not only in bookkeeping.

This is where cash flow forecasting becomes more than a finance task. It becomes a practical tool for spotting pressure early and making better decisions under uncertainty.

Cash flow forecasting helps leaders move from financial movement to better decisions by tracking cash in, cash out, timing gaps, and likely pressure points.

What should you put into a cash flow forecast?

The simplest answer is: all the major cash coming in, all the major cash going out, and the timing of both.

A forecast does not need to be complicated to be useful. In fact, if it becomes too complicated, people often stop updating it. And a beautiful forecast nobody updates is about as useful as a gym membership used once in January.

Start with the numbers you already trust

Begin with the figures that are closest to reality:

- opening bank balance

- sales history

- unpaid invoices

- known customer payment dates

- supplier bills

- payroll

- rent

- loan repayments

- software subscriptions

- insurance

- tax liabilities

This is one area where the better practical guides are consistent. Start with the known figures, then add careful estimates where needed. The British Business Bank guide, FreeAgent’s guide, and the UK government template all point strongly in this direction.

The goal is not a heroic act of prediction. The goal is an honest working model.

Which cash outflows are easiest to miss?

In my experience, the most dangerous forecast errors are often not dramatic. They are ordinary costs that were easy to forget.

These commonly include:

- VAT

- PAYE

- National Insurance

- Corporation Tax

- annual insurance renewals

- rent reviews

- equipment purchases

- one-off repairs

- stock buys

- professional fees

- software renewals

Miss one or two large outflows and the forecast can suddenly look much healthier than reality.

That is one reason templates from organisations like Start Up Loans, ACCA, and Barclays are useful reference points. They remind you that forecasting is not just about sales optimism. It is also about remembering the cash that leaves quietly but reliably.

How far ahead should you forecast?

That depends on the decision.

For short-term control, many businesses benefit from a 13-week cash flow forecast. It is close enough to be useful and far enough to spot pressure building.

For broader planning, a monthly forecast looking six to twelve months ahead can help with hiring, investment, and growth decisions.

If cash is tight, update it weekly. If the business is more stable, monthly may be enough. Xero recommends updating forecasts at least monthly, or more often when cash is under pressure. That is sensible advice.

The main point is not the exact format. It is keeping the view current.

How do you build a forecast that is realistic, not hopeful?

This is where many forecasts go wrong.

They are not built from likely reality. They are built from a version of reality the business would very much like to happen.

Hope is useful in life. It is less helpful in a cash flow model.

Use current trading patterns, not wishful thinking

Base your forecast on what the business is actually doing now.

Look at:

- recent sales patterns

- real payment timings

- average customer delays

- current supplier terms

- upcoming tax dates

- fixed costs you already know are coming

If your business has been growing slowly, do not suddenly project a leap without a very clear reason. If customers usually pay late, do not assume they will all become saints next month.

What I have seen is that over-optimistic sales assumptions are one of the fastest ways to make a forecast look comforting and become useless.

Build in late payments instead of assuming perfect timing

This is one of the most practical improvements you can make.

Instead of assuming every invoice will be paid on the agreed date, test the forecast using more realistic delays.

For example:

- 7 days late

- 14 days late

- 30 days late

That gives you a more honest picture of cash availability.

It also reflects real business life far better. Xero already notes that customers may pay 30 to 90 days after an invoice is issued, which makes timing central, not optional.

Keep the structure simple enough to update regularly

A useful forecast is one you will keep using.

That means:

- major income lines

- major cost lines

- clear timing columns

- short notes for unusual items

- no unnecessary complexity

If the forecast becomes too clever, it often becomes neglected.

And once it is neglected, it stops being a decision tool and becomes a historical artefact.

A realistic forecast is usually more useful than an impressive one. In my experience, the best cash flow models are simple enough to update, honest enough to trust, and clear enough to guide action.

How can you plan for uncertainty without making the forecast too complex?

A good forecast should not assume that everything will go exactly to plan.

That would be nice. It would also be fantasy!

The practical answer is not to build a huge complicated model. It is to build a sensible forecast with a few useful pressure tests.

Should you use best case, normal case, and worst case scenarios?

Yes, usually.

A three-scenario view is one of the simplest ways to make the forecast more useful.

For example:

Best case

- sales improve

- debtors pay on time

- costs stay stable

Normal case

- sales stay near current levels

- payment timing remains typical

- costs move as expected

Worst case

- one large customer pays late

- sales soften

- supplier or wage costs rise

This gives you a range of likely outcomes rather than one neat line pretending the future has signed a contract.

How do you allow for late payments and cost increases?

Use timing shifts and pressure assumptions.

Ask:

- what happens if our top customer pays 30 days late?

- what happens if supplier costs rise by 5%?

- what happens if sales dip for six weeks?

- what happens if VAT hits while cash is already tight?

This is where forecasting becomes especially useful under uncertainty. It helps you see the consequences before they arrive.

How do seasonality and busy periods change the picture?

Even strong businesses often have uneven cash flow.

Retail has Christmas peaks.

Some service firms slow in summer.

Schools, holidays, and sector cycles create predictable changes.

Tax dates create lumpy outflows.

Stock-heavy businesses often spend cash before the sales arrive.

This is one reason seasonal reality needs to be built into the forecast rather than treated as an annoying surprise.

How should leaders use the forecast every month?

The biggest mistake is to treat the forecast as a document you prepare, admire, and forget.

A forecast is most useful when it becomes part of the monthly rhythm of the business.

Compare forecast figures with actual results

This is one of the most useful habits.

Check:

- what did we expect?

- what actually happened?

- why was there a gap?

That gap is often where the learning sits.

Maybe sales timing was slower.

Maybe costs landed earlier.

Maybe a big invoice stayed unpaid.

Maybe your assumptions were simply too optimistic.

That is not failure. That is useful feedback.

Keep a rolling cash flow view

Do not let the forecast end at the edge of the spreadsheet!

Keep it moving forward.

A rolling 13-week view can help with short-term control.

A monthly forward view can support broader planning.

As new information arrives, update the forecast and push the view forward again.

That keeps the model alive and relevant.

Use the forecast to decide when to spend, pause, chase, or borrow

This is where leadership judgment comes in.

A forecast should support decisions such as:

- whether now is the right time to hire

- whether to delay equipment spending

- whether to push harder on debt collection

- whether to pause discretionary spending

- whether to ask for finance before the pressure becomes urgent

This connects closely to how I think about decisions more broadly in the KrisLai Decision Framework™. Better decisions come from understanding behaviour, signals, environment, and consequences. Cash flow forecasting gives you signals. The decision quality depends on how you use them.

What this looks like in real business

Let’s make it practical.

A small service business may look busy and profitable but still face cash pressure because clients pay late. In that case, the forecast may show that hiring now would increase pressure unless debtor collection improves first.

A retail business may need to buy stock well before the busy season. The forecast may show that the real pressure point is not the stock purchase itself, but the weeks between buying it and selling it.

A growing business may see strong sales and assume expansion is affordable. The forecast may show that runway is shorter than expected once payroll, tax, and slower-paying customers are factored in.

Good businesses often run into cash pressure not because they are failing, but because timing, growth, and payment behaviour are harder to manage than expected. A cash flow forecast helps you see that earlier.

Where this goes wrong

This is worth saying plainly.

Cash flow forecasting often fails for very ordinary reasons.

- sales assumptions are too hopeful

- major outflows are missed

- invoices are assumed to be paid on time

- the model is too complex to update

- the forecast is created for a lender but not used internally

- nobody checks forecast versus actual

- the document exists, but the business does not act on it

In my experience, one of the most common mistakes is this: the forecast becomes a reporting exercise instead of an early-warning decision tool.

That is a waste of one of its biggest strengths.

- The forecast is hopeful rather than realistic

- Tax, timing, and late payments are underplayed

- It is built once and not updated

- It explains the past but does not guide the next decision

- It looks tidy in a file but changes nothing in the business

What you should actually do

If you want a stronger cash flow process, I would start here:

- Use real numbers first

Start with bank balances, unpaid invoices, known bills, payroll, rent, and tax dates. - Build around timing, not just totals

Ask when cash will actually arrive and leave. - Create one honest base case

Not your dream month. Your realistic one. - Add simple scenario pressure

Late payments, softer sales, higher costs. - Review forecast versus actual regularly

That is where the learning happens. - Keep it rolling

Update it as new information comes in. - Use it to guide decisions

Hiring, stock, spending, borrowing, and debt collection should all connect back to the forecast.

This is not glamorous work.

It is, however, very good business thinking.

If you want to turn this into something practical, I’ve put together a free Cash Flow Forecast Template you can use to track timing gaps, test pressure points, and make better decisions before cash problems become urgent.

Free Download: Cash Flow Forecast Template for Better Decisions

Cash flow forecasting is most useful when it helps you act before pressure becomes a problem.

Enter your email below and I’ll send you the free spreadsheet template, designed to help you track cash in, cash out, timing gaps, and likely pressure points with more clarity and confidence.

This practical template is built to support better business decisions under uncertainty.

Conclusion and Final Thoughts

Cash flow forecasting helps you move from guesswork to clearer action.

It helps you see whether cash is likely to be available when the business needs it. It helps you plan for timing gaps, late payments, tax outflows, and uneven trading. Most importantly, it helps you make decisions earlier, with more confidence, and with fewer nasty surprises.

What I have seen is that the strongest forecasts are not the most complicated ones. They are the ones that are realistic, updated often, and built around actual cash timing.

That is what makes them useful.

And that is why cash flow forecasting is not just a finance exercise. It is a practical leadership tool for making better decisions under uncertainty.

PS: If you want to strengthen your financial decision-making further, review this alongside your work on working capital, financial ratios, and financial dashboards. These are all part of seeing the business more clearly before pressure forces your hand.

Frequently Asked Questions

What is cash flow forecasting?

Cash flow forecasting is the process of estimating how much cash will come into and leave the business over a future period, so you can see whether there is likely to be enough money available when bills fall due.

What is the difference between profit and cash flow?

Profit shows whether the business is making money on paper. Cash flow shows whether money is actually available at the right time. A business can be profitable and still run short of cash if payments arrive late or costs land early.

How often should a cash flow forecast be updated?

It depends on the business, but monthly is a sensible minimum. If cash is tight or conditions are changing quickly, weekly updates are often more useful.

What should be included in a cash flow forecast?

A forecast should include opening cash balance, expected cash inflows, expected cash outflows, tax payments, payroll, supplier bills, loan repayments, and any large one-off items that affect timing.

Why are cash flow projections useful for small businesses?

Cash flow projections help small businesses spot shortfalls early, plan spending more safely, prepare for late payments, and make better decisions about hiring, stock, investment, and finance.

About the author

Kris Lai is a business operator and managing director with experience in land and building surveying, facilities management, logistics, and service delivery.

Earlier in his career, he worked as a Search Engine Evaluator (via Lionbridge, supporting Google), where he assessed search result relevance, user intent, and content quality using structured evaluation frameworks. This experience gives him a rare, practical understanding of how search systems interpret signals and make ranking decisions.

In parallel, whilst working with a charity organisation, he has delivered 1000’s of structured presentations in English, Finnish, and Chinese to audiences ranging from small groups to more than 600 people, and has spent decades mentoring and developing others. This experience informs his approach to clarity, communication, and decision-making under pressure.

He writes about AI, search behaviour, business strategy, and decision-making from a practical, real-world perspective.

If you enjoy exploring the ideas behind better business decisions, you may find the Business Thinking Hub useful.

👉 Explore ideas connected to better business decisions:

- How AI Is Changing Search Behaviour (And What Businesses Must Do Now)

- Decision-Making Framework Examples: The KrisLai Method in Action

- The KrisLai Decision Framework: A Better Way to Make Business Decisions

- Micro vs Macro Marketing: When to Target Broad Audiences vs Niche Customers

- Customer Intent Marketing: How to Turn Buying Signals Into Sales