Financial statements are more than accounting reports. Read well, they help managers understand performance, cash pressure, risk, and the financial consequences of business decisions. This guide explains the main statements, how they connect, and the common traps that lead people to misread the numbers.

Disclosure: If you click on my affiliate/advertiser’s links, I may receive a tiny commission. AND… Most of the time, you will receive an offer of some kind. It’ s a Win/Win!

What this article covers

In this article, I will explain what financial statements are, what the main statements show, how to read them together, how managers often misread the numbers, and how financial statements can support better decisions in real business.

I will also cover simple ratios, warning signs, UK business relevance, and how AI can help with analysis without replacing human judgement.

This article is based on practical business thinking, independent research, and my own analysis and synthesis of how financial information, behaviour, strategy, and decision-making affect real business results.

Financial statements are not just for accountants.

They are business signals.

That is the first thing I would say to any manager, owner, or non-finance leader who feels slightly nervous around accounts.

You do not need to become an accountant to understand financial statements. But you do need to understand what the numbers are trying to tell you.

In my experience, many poor business decisions do not come from ignoring financial statements completely. They come from reading them too narrowly.

A manager sees rising sales and assumes the business is healthy.

An owner sees profit and assumes there is enough cash.

A leader sees assets on the balance sheet and assumes risk is low.

In real business, the question is not only:

“What do the numbers say?”

A better question is:

“What decision should these numbers improve?”

That is where financial statements become useful.

They help you decide whether to hire, spend, borrow, cut costs, raise prices, chase overdue invoices, review strategy, or slow down before a mistake becomes expensive.

Better decisions come from understanding behaviour, signals, environment, and consequences.

I write about how better decisions are made in business — combining strategy, behaviour, and practical thinking.

Key ideas

- Financial statements are business signals, not just accounting reports.

- One statement alone never tells the full story.

- Profit and cash are not the same thing.

- Managers often misread financials when they focus on one number in isolation.

- Financial statements are most useful when they improve real decisions.

What are financial statements?

Financial statements are formal reports that show how a business is performing, what it owns and owes, how cash is moving, and how ownership value has changed.

The main financial statements are usually:

- the balance sheet

- the income statement, also called the profit and loss account

- the cash flow statement

- the statement of changes in equity

Each one answers a different money question.

The balance sheet asks:

“What does the business own, and what does it owe?”

The income statement asks:

“Did the business make a profit over this period?”

The cash flow statement asks:

“Where did the money actually come from and go?”

The statement of changes in equity asks:

“How has the ownership value changed?”

For UK businesses, financial statements also matter because they connect to statutory accounts, directors’ responsibilities, Companies House, HMRC, lenders, investors, and business planning.

But for day-to-day business thinking, the most important point is this:

Financial statements are not only there to satisfy paperwork. They should help you understand the business better.

Financial statements, in simple terms

Financial statements are reports that show how a business is performing, what it owns and owes, how cash is moving, and how the value of ownership has changed.

Why one statement alone never tells the full story

This is one of the biggest traps.

A single financial statement can give you part of the picture, but not the whole picture.

For example:

- a business can be profitable but short of cash

- sales can grow while margins fall

- assets can look strong while debt rises

- cash can improve because the business borrowed money, not because trading improved

- profit can rise because of a one-off gain, not because the core business is stronger

That is why managers should read financial statements together.

A balance sheet without a cash flow statement can be misleading.

An income statement without the balance sheet can hide risk.

A cash flow statement without the income statement can make short-term cash movement look better or worse than the business really is.

In other words, the statements work as a set.

Not as isolated pieces of paper.

What do the main financial statements show?

Let us keep this practical.

You do not need complex accounting language to understand the basic job of each statement.

The balance sheet shows what a business owns and owes

The balance sheet is a snapshot of the business at a specific date.

It shows:

- assets — what the business owns or controls

- liabilities — what the business owes

- equity — the owner’s or shareholders’ remaining interest in the business

The basic balance sheet rule is:

Assets = Liabilities + Equity

Simple examples of assets include:

- cash

- stock

- equipment

- vehicles

- property

- money owed by customers

- computers or tools

Simple examples of liabilities include:

- supplier bills

- loans

- overdrafts

- tax owed

- lease obligations

- wages owed

- credit card balances

Equity is what is left for the owners after liabilities are taken away from assets.

In plain English:

If the business sold everything it owned and paid everything it owed, equity is the part that would theoretically belong to the owners.

Of course, real life is messier than that.

Assets may not sell for the value shown.

Debtors may not pay.

Stock may be old.

Equipment may be worth less than expected.

That is why the balance sheet needs judgement, not just reading.

The income statement shows whether the business made a profit

The income statement, or profit and loss account, shows performance over a period of time.

That period might be a month, a quarter, or a year.

It usually shows:

- revenue or sales

- cost of sales

- gross profit

- operating expenses

- operating profit

- finance costs

- tax

- profit or loss

The key thing to understand is this:

sales are not profit!

A business can sell a lot and still make very little money.

For example, if sales rise but costs rise faster, profit may fall.

A business can also look busy while still being financially weak.

That is why revenue alone is a dangerous comfort blanket.

Revenue tells you activity.

Profit tells you whether that activity is leaving something behind.

The cash flow statement shows where the money really went

The cash flow statement is often where reality appears.

That is because profit and cash are not the same thing.

A business can show profit but still struggle for cash if:

- customers have not paid yet

- stock has been bought in advance

- large bills are due

- loan payments are high

- tax payments are coming

- money is tied up in work in progress

The cash flow statement usually separates cash into three areas:

- operating cash flow — cash from normal trading

- investing cash flow — cash spent on or received from assets and investments

- financing cash flow — cash from loans, repayments, shares, or dividends

For managers, operating cash flow is especially important.

If the core business is not producing cash, that is a signal worth noticing.

A profitable business with weak operating cash flow needs careful attention.

The statement of changes in equity shows how ownership value moved

This statement is often less familiar to non-accountants, but it still matters.

It explains changes in equity over time.

That may include:

- retained profit

- losses

- dividends

- new shares

- share buybacks

- reserves

- other adjustments

In simpler terms, it helps show how the owners’ stake in the business changed during the period.

For many small business readers, this may not be the first statement they study. But it still forms part of the full picture, especially when looking at growth, dividends, retained earnings, or changes in ownership structure.

How should managers read financial statements without getting lost?

If you are not an accountant, financial statements can feel overwhelming.

The trick is not to read every line with equal intensity at first.

Start with a simple order.

A simple order for reading financial statements

- Start with the income statement to understand sales, costs, and profit.

- Check the balance sheet to see assets, liabilities, and equity.

- Read the cash flow statement to see whether money is actually moving well.

- Review the notes to understand context, risks, and accounting details.

- Look for trends rather than relying on one year alone.

Start with trends, not one year’s figures

One year’s figures can mislead.

Trends are usually more useful.

Ask:

- Is revenue growing or falling?

- Is profit improving or weakening?

- Are costs rising faster than sales?

- Is cash improving or getting tighter?

- Is debt increasing?

- Are margins stable?

- Are customers taking longer to pay?

- Is stock increasing faster than sales?

A single year can be affected by one-off events.

A trend tells you more about direction.

And in business, direction often matters more than one impressive number.

Read profit, cash, and debt together

This is a simple but powerful habit.

Do not look at profit alone.

Ask:

- Is the business profitable?

- Is it generating cash?

- Is debt rising or falling?

- Are short-term bills covered?

- Is growth consuming too much cash?

- Are customers paying on time?

A business may show profit while cash is under pressure.

Another business may show lower profit because it has invested for future growth.

Numbers need context.

That is why financial analysis is not only about calculation. It is about interpretation.

Read the notes, not just the headline numbers

This is where many non-finance readers stop too early.

The notes to the accounts may explain important details, such as:

- accounting policies

- leases

- loan terms

- related-party transactions

- unusual costs

- tax issues

- commitments

- risks

- assumptions

- one-off items

Headline figures can look clean.

The notes often explain what is underneath.

If you skip the notes, you may miss the most important part of the story.

How managers misread financial statements

This is where financial statements become a decision issue.

What I’ve seen go wrong is rarely because someone looked at the accounts and understood them too well.

It is usually because they saw one number, liked or disliked it, and built a decision around it too quickly.

What I’ve seen go wrong

In my experience, managers often misread financial statements when they look at one number in isolation. Revenue, profit, cash, debt, and margins need to be read together. A business can look successful on one statement and still be under pressure elsewhere.

Mistake 1 — Confusing profit with cash

This is probably the most common mistake.

A business makes a sale.

The income statement may show revenue.

But if the customer has not paid yet, the cash is not in the bank.

Now imagine the business also needs to pay wages, suppliers, rent, tax, and loan repayments.

The accounts may show profit.

The bank account may still feel painful.

That is why cash flow matters so much.

Profit is important.

But cash keeps the business breathing.

Mistake 2 — Seeing revenue growth and assuming the business is healthy

Growing sales can be exciting.

But sales growth does not automatically mean the business is improving.

Revenue can rise while:

- margins fall

- costs increase

- cash collection worsens

- debt rises

- staff become overstretched

- customer complaints increase

- low-quality customers create more work than profit

In real business, growth can be good.

But poor-quality growth can create pressure.

That is why managers should ask:

“Is this growth profitable, cash-positive, and sustainable?”

Not just:

“Are sales up?”

Mistake 3 — Ignoring working capital

Working capital sounds technical, but the idea is simple.

It is about the money tied up in everyday operations.

For example:

- stock sitting on shelves

- customers who owe money

- suppliers waiting to be paid

- cash needed to keep the business moving

A business can be profitable and still struggle if too much money is tied up in stock or unpaid invoices.

This matters especially for small businesses.

A few slow-paying customers can create real pressure.

Mistake 4 — Missing what the notes are telling you

Sometimes the most important information is not in the main table.

It is in the notes.

The notes may reveal:

- unusual income

- unusual costs

- accounting assumptions

- lease obligations

- debt terms

- risks

- commitments

- changes in accounting treatment

If a manager only reads the headline numbers, they may miss the detail that changes the decision.

Mistake 5 — Looking at the accounts without asking what behaviour created them

This is one of the most important points.

Financial statements do not appear by magic.

They are the result of behaviour.

For example:

- late-paying customers affect cash

- poor pricing affects margins

- over-ordering affects stock

- weak invoicing affects debtor days

- poor cost control affects profit

- unclear ownership affects spending

- slow decisions affect investment

That is why I do not see financial statements as only finance documents.

They are behavioural evidence.

They show what people, customers, suppliers, managers, and systems have been doing.

The decision traps in financial analysis

The numbers may be correct, but the conclusion can still be wrong.

That is why decision traps matter.

Trap 1 — “The business is profitable, so we can afford it”

Profit does not always mean spare cash.

Before hiring, buying equipment, or taking on a new commitment, look at cash flow, debt, payment timing, and upcoming obligations.

A business can make a profit and still struggle to pay bills on time.

Trap 2 — “Sales are up, so the strategy is working”

Sales growth is only one signal.

A strategy may still be weak if:

- margins are shrinking

- customer acquisition costs are too high

- the wrong customers are being attracted

- service quality is falling

- cash flow is worsening

- the team is overloaded

Good strategy is not just about more activity.

It is about better results.

Trap 3 — “Cutting costs always improves performance”

Cost-cutting can help.

But cutting the wrong costs can damage the business.

For example, cutting training may save money today but reduce quality later.

Cutting customer support may improve short-term profit but increase complaints.

Cutting marketing may protect cash now but weaken future demand.

The better question is not simply:

“What can we cut?”

It is:

“What cost is waste, and what cost supports value?”

Trap 4 — “The balance sheet looks strong, so risk is low”

A balance sheet can look strong and still hide pressure.

Ask:

- Are assets easy to turn into cash?

- Are customers paying on time?

- Are liabilities due soon?

- Is debt affordable?

- Is stock still sellable?

- Are assets overvalued?

- Is cash enough for the next few months?

A strong-looking balance sheet still needs careful reading.

Trap 5 — “AI says the accounts look healthy”

AI can be useful.

It can summarise accounts, spot patterns, compare figures, draft questions, and help non-finance managers understand unfamiliar terms.

But AI can also miss context.

It may not understand your customers, your cash cycle, your supplier relationships, your risks, or what is hidden in the notes.

AI can help you read financial statements faster.

It should not take responsibility for the decision!

How financial statements support better decisions

The real value of financial statements is not in reading them once a year and filing them away.

The real value is in using them to make better decisions.

Hiring decisions

Before hiring, ask:

- Can the business afford the full cost?

- Is the cash flow strong enough?

- Will this role generate value?

- What happens if sales slow down?

- Is the need temporary or long-term?

A new salary is not just one monthly figure.

It is a commitment.

Financial statements help you judge whether that commitment is sensible.

Pricing decisions

If margins are falling, the answer may be pricing.

Or it may be costs.

Or customer mix.

Or poor efficiency.

Financial statements help you see whether the business is busy but not profitable.

That is one of the most dangerous places to be.

Spending decisions

Before a major purchase, ask:

- Will this improve productivity?

- Will it reduce costs?

- Will it strengthen capacity?

- Will it create cash pressure?

- Is the timing right?

- What else could this money do?

A purchase may be useful and still badly timed.

Funding decisions

Borrowing can help a business grow.

It can also add pressure.

Financial statements help you judge whether funding will strengthen the business or simply cover a weakness that needs solving another way.

Strategy decisions

Financial statements can test whether strategy is working.

For example:

- Are the most profitable services getting enough attention?

- Are new offers improving margins?

- Is growth creating cash pressure?

- Are costs aligned with priorities?

- Is the business model becoming stronger or weaker?

Strategy should not live only in planning documents.

It should show up in the numbers.

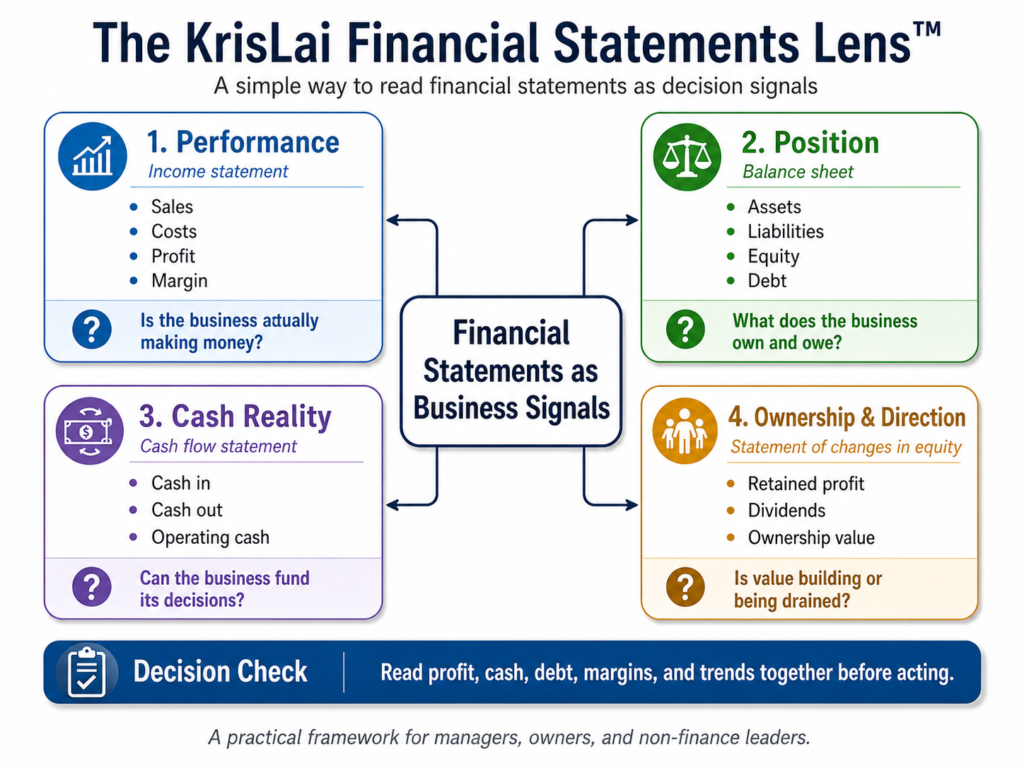

The KrisLai Financial Statements Lens™

- Behaviour – what customer, supplier, staff, or management behaviour is affecting the numbers?

- Signals – what do margins, cash flow, debt, and working capital reveal?

- Environment – what market, cost, credit, or regulation pressures are shaping the figures?

- Consequences – what happens if you misread the numbers and act too soon, too late, or in the wrong place?

Better decisions come from understanding behaviour, signals, environment, and consequences.

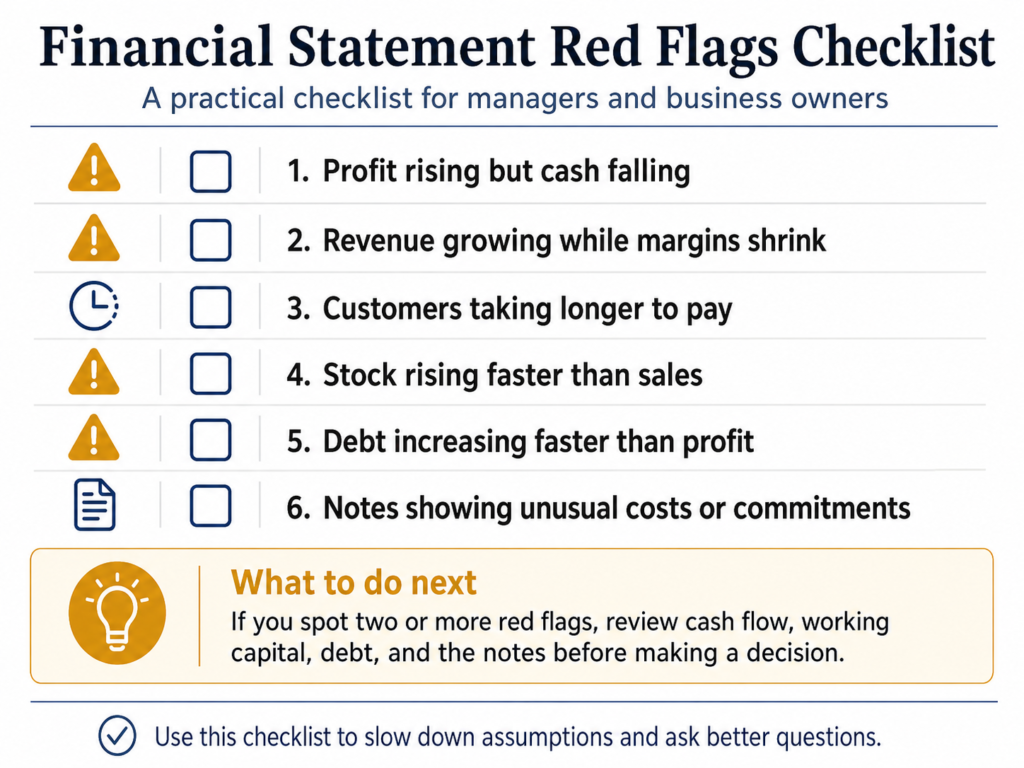

Simple ratios and red flags worth watching

You do not need to become a finance expert to use a few simple checks.

Ratios are not magic.

They are signals.

They help you ask better questions.

Profit margin

Profit margin shows how much profit is left after costs.

If sales are rising but profit margin is falling, something needs attention.

Possible causes include:

- higher supplier costs

- weak pricing

- discounting

- inefficient delivery

- rising wages

- poor customer mix

Current ratio

The current ratio compares short-term assets with short-term liabilities.

In simple terms, it helps show whether the business may be able to cover its short-term bills.

It is not perfect, because some assets are easier to turn into cash than others.

But it can still be a useful warning sign.

Operating cash flow

Operating cash flow shows whether the core business is bringing in cash.

If profit looks fine but operating cash flow is weak, look closer.

The business may have problems with:

- slow-paying customers

- too much stock

- rising costs

- poor payment terms

- weak cash collection

Debt levels

Debt is not always bad.

Used well, it can support growth.

Used badly, it can create pressure.

Watch whether debt is:

- rising faster than profit

- difficult to service

- used to cover trading weakness

- hiding poor cash flow

- creating short-term pressure

Debtor days or unpaid invoices

If customers are taking longer to pay, the business may look healthy on paper while cash becomes tight.

This is one of the most practical checks for small businesses.

A sale is not fully useful if the money never arrives.

Why financial statements matter for UK businesses in 2026

For UK businesses, financial statements matter in more than one way.

They help with compliance.

They help with tax and filing.

They help directors understand the business.

They also help banks, investors, suppliers, and business partners judge whether the business is stable and trustworthy.

They help you stay compliant and file the right information

Companies need proper accounts for reporting and filing.

Directors also have responsibilities around financial information.

For small businesses, this may involve working with an accountant, filing with Companies House, dealing with HMRC, and keeping records accurate enough to support decisions and obligations.

Even if an accountant prepares the statements, the owner or director should still understand the main story.

You cannot lead well if the numbers are a complete mystery.

They build trust with banks, suppliers, and investors

Clear financial statements can support:

- loan applications

- credit terms

- supplier confidence

- investor conversations

- grant applications

- business valuations

- partnership discussions

Clean, consistent accounts often matter more than flashy numbers.

A bank or supplier may not expect perfection.

But they will want to see reliability, clarity, and control.

They support better leadership

Leadership is not only about people and vision.

It also includes understanding whether the business can afford its choices.

A leader does not need to do every calculation.

But they should be able to ask:

- are we profitable?

- are we cash healthy?

- what risks are growing?

- what does the balance sheet show?

- what is changing over time?

- what decision do these numbers support?

That is practical leadership.

Not finance for finance’s sake.

Finance for better judgement.

Final thought: financial statements are business signals, not just reports

Financial statements become more useful when they are read together, compared over time, and connected to real business behaviour.

The balance sheet, income statement, cash flow statement, and statement of changes in equity each tell part of the story.

But the real value comes from asking better questions:

- What is changing?

- Why is it changing?

- What risk is growing?

- What behaviour created the numbers?

- What decision needs to improve?

- What happens if we ignore the warning signs?

That is how financial statements become a decision tool.

Not just an accounting document.

In real business, the numbers do not make the decision for you.

But they can help you see more clearly.

And when you see more clearly, you are far less likely to make expensive assumptions.

As the Finnish saying goes, “ei savua ilman tulta” – There is no smoke without fire.

Financial statements often show the smoke.

Good judgement asks where the fire may be.

Final takeaway

Financial statements are most useful when they help managers make better decisions. Read profit, cash, debt, margins, and trends together. Then ask what the numbers reveal about behaviour, risk, strategy, and the choices the business needs to make next.

Related reading on KrisLai.com

- Related article: Business Acumen Skills

- Glossary or definition article: Problem-Solving in Business

- Pillar topic: Business Thinking Hub

- Decision-Making Framework Examples

- Business Strategy Planning

- Scenario Planning in Business

- Human Resource Management

Frequently Asked Questions About Financial Statements

What are financial statements?

Financial statements are formal reports that show how a business is performing, what it owns and owes, how cash is moving, and how ownership value has changed.

What are the four main financial statements?

The four main financial statements are the balance sheet, income statement, cash flow statement, and statement of changes in equity. Together, they show financial position, performance, cash movement, and ownership changes.

How do you read financial statements as a beginner?

Start by reading the income statement to understand sales and profit, then check the balance sheet for assets and liabilities, review the cash flow statement for cash movement, and read the notes for context.

What is the difference between profit and cash flow?

Profit shows whether income was higher than costs over a period. Cash flow shows whether money actually moved in and out of the business. A business can be profitable but still short of cash.

Why do managers misread financial statements?

Managers often misread financial statements when they focus on one number alone, such as sales or profit, without also checking cash flow, debt, margins, working capital, and the notes to the accounts.

What financial statement red flags should business owners watch for?

Useful warning signs include falling margins, weak operating cash flow, rising debt, slow-paying customers, increasing stock levels, growing liabilities, and sales growth that does not turn into profit or cash.

How can financial statements help business decision-making?

Financial statements help managers make better decisions about hiring, pricing, spending, borrowing, investment, and strategy by showing the financial consequences and risks behind business choices.

About the author

Kris Lai is a business operator and managing director with experience in land and building surveying, facilities management, logistics, and service delivery.

Earlier in his career, he worked as a Search Engine Evaluator (via Lionbridge, supporting Google), where he assessed search result relevance, user intent, and content quality using structured evaluation frameworks. This experience gives him a rare, practical understanding of how search systems interpret signals and make ranking decisions.

In parallel, whilst working with a charity organisation, he has delivered 1000’s of structured presentations in English, Finnish, and Chinese to audiences ranging from small groups to more than 600 people, and has spent decades mentoring and developing others. This experience informs his approach to clarity, communication, and decision-making under pressure.

He writes about AI, search behaviour, business strategy, and decision-making from a practical, real-world perspective.

If you enjoy exploring the ideas behind better business decisions, you may find the Business Thinking Hub useful.

👉 Explore ideas connected to better business decisions:

- How AI Is Changing Search Behaviour (And What Businesses Must Do Now)

- Decision-Making Framework Examples: The KrisLai Method in Action

- The KrisLai Decision Framework: A Better Way to Make Business Decisions

- Micro vs Macro Marketing: When to Target Broad Audiences vs Niche Customers

- Customer Intent Marketing: How to Turn Buying Signals Into Sales