Working capital is not just a finance term. It is one of the clearest early warning systems in business. When customers pay more slowly, stock sits too long, or supplier pressure starts to build, working capital often shows the strain before cash problems become obvious.

Working capital trouble rarely arrives with a brass band and a warning sign!

It usually starts quietly.

A few customers take longer to pay. Stock builds up a little more than planned. A supplier wants paying sooner. Someone says, “We’re profitable, so we’re fine,” which is often the business version of whistling past the graveyard.

That is why I think working capital matters so much.

In simple terms, working capital is the money tied up in the day-to-day running of the business. It sits in the space between what is coming in, what is going out, and when those two things happen. If that balance starts to slip, the pressure often shows up here before it becomes a full cash problem. British Business Bank, Investopedia, and other leading explainers all frame working capital as the difference between current assets and current liabilities, and as a core measure of short-term financial health.

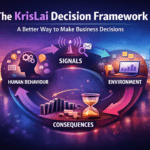

This approach is part of the KrisLai Decision Framework, a practical method for improving business decisions. Better decisions come from understanding behaviour, signals, environment, and consequences. Working capital is one of those signals. It tells you when timing is drifting, when operating pressure is building, and when the business may be less steady than the profit figure suggests.

I write about how better decisions are made in business — combining strategy, behaviour, and practical thinking. That is exactly how I want to treat this topic. Not as a dry finance definition. As a practical leadership issue.

Working capital is the difference between a business’s current assets and current liabilities. In plain English, it helps show whether the business has enough short-term resources to meet its short-term obligations and keep operating smoothly.

- Working capital is often an early warning sign, not a late one.

- A profitable business can still run into pressure if timing goes wrong.

- Receivables, stock, and payables are not just finance items. They are decision signals.

- Smart leaders watch working capital before cash gets tight, not after.

- Good judgement matters most when the future is unclear.

What is working capital, in plain English?

Working capital is the gap between what the business owns in the short term and what it owes in the short term.

That is the formal answer.

The practical answer is simpler: working capital helps show how much room the business has to keep moving without cash strain.

The standard formula is:

Working Capital = Current Assets – Current Liabilities

Current assets usually include:

- cash

- accounts receivable

- inventory

- short-term items that can be turned into cash within a year

Current liabilities usually include:

- accounts payable

- short-term borrowing

- tax due

- payroll obligations

- other bills due within a year

That is the same core definition used by British Business Bank, Investopedia, SumUp, Square, and Wikipedia.

What is the working capital formula?

The working capital formula is:

Current Assets – Current Liabilities

If your business has:

- £120,000 in current assets

- and £80,000 in current liabilities

then working capital is £40,000.

That suggests some short-term breathing room.

If the result is negative, that can be a warning sign. But even then, context matters. Some business models run with lower working capital more comfortably than others. Investopedia and SumUp both point out that what counts as “healthy” working capital can vary by industry and business model.

What does positive or negative working capital actually mean?

Positive working capital usually means the business has enough short-term resources to cover short-term obligations.

Negative working capital can mean the opposite: pressure, strain, or a growing risk that the business may struggle to meet short-term commitments.

But I would be careful here.

A simple formula is useful, but it is not the whole story. What matters is not only the number, but why it looks the way it does.

For example:

- is stock too high?

- are customers paying more slowly?

- are suppliers being paid too quickly?

- is short-term borrowing growing?

- is the business expanding faster than cash can support?

That is where the real judgement begins.

What does the working capital ratio tell you?

The working capital ratio takes the same idea and expresses it as:

Current Assets / Current Liabilities

A ratio below 1 can suggest that short-term obligations are starting to crowd out short-term resources. British Business Bank and iwoca both highlight this as a sign that a business may struggle to meet short-term commitments.

But there is a useful twist here!

A very high ratio is not always wonderful either. It can mean too much cash is trapped in stock, receivables, or underused resources. iwoca makes this point clearly: very high working capital can signal inefficiency as well as safety.

So the goal is not “more working capital at all costs.”

The goal is healthy, usable, well-managed working capital.

Why is working capital often the first warning sign, not the last?

Working capital is often the first warning sign because cash problems usually start with timing and behaviour, not drama.

That is one reason I think leaders should watch it early.

A cash crisis rarely begins when the bank balance is already collapsing. It usually begins when small shifts start to build:

- customers take longer to pay

- stock stays on the shelf longer

- suppliers push for quicker payment

- short-term borrowing becomes a little more frequent

- the business starts leaning harder on timing rather than strength

British Business Bank is especially clear on one important point: a business can appear profitable but still fail if it cannot meet short-term obligations when they fall due. That is the heart of the issue.

Why can a business look profitable while cash still gets tight?

Because profit and cash are not the same thing.

You can make a sale today, count the revenue, and still not receive the money for weeks. Meanwhile, payroll, rent, tax, supplier invoices, and loan repayments keep marching in as if nothing could possibly go wrong.

This is why working capital and cash flow are closely linked, but not identical.

A business may look healthy on paper while cash starts running short in real life. That is one reason this article connects closely to my wider work on cash flow forecasting, financial dashboards, and financial ratios. These are all ways of spotting pressure before it becomes expensive.

What usually changes first when pressure starts to build?

Usually, small things change first.

In my experience, leaders often notice one or more of these before the full problem is obvious:

- accounts receivable take longer to collect

- inventory and working capital drift higher because stock is not moving

- accounts payable and working capital become tighter as suppliers push harder

- short-term borrowing gets used more often

- the working capital cycle slows down

- staff spend more time “managing around” the pressure

- decisions start becoming reactive

That is why I see working capital as a signal system. It tells you something about the health, rhythm, and strain of the business before the formal crisis arrives.

Working capital is not only a number. It is a pattern. It shows how cash, inventory, customer behaviour, supplier timing, and day-to-day pressure are interacting inside the business.

A simple way to think about working capital is as a signal loop. Small changes in payment timing, stock, and supplier pressure build into either resilience or strain, depending on how leaders respond.

The Working Capital Signal Loop

Customer payments

↓

Stock movement

↓

Supplier timing

↓

Working capital pressure

↓

Leadership decision

↓

Cash resilience or cash strain

Which working capital decisions matter most in real business?

The most important working capital decisions usually sit around receivables, stock, and payables.

That sounds simple, but these are not just finance settings. They are real-world judgement calls about risk, resilience, relationships, and control.

How fast are customers paying, and what should you do when they are not?

This is one of the biggest practical working capital questions.

If customers pay slowly, the business carries the strain. That may not be visible immediately, but it builds over time.

So I would ask:

- are invoices being chased early enough?

- are payment terms sensible?

- are credit checks being used properly?

- are some customers becoming habitual late payers?

- is the team avoiding hard conversations because they do not want to upset the relationship?

This is where behavioural insight matters. Late payment is not always just a finance issue. Sometimes it reflects weak process, unclear ownership, poor habits, or reluctance to act.

What I have seen is that businesses often let this drift because each delayed payment looks manageable on its own. Then the pattern becomes a problem.

How much stock should you hold before it starts tying up too much cash?

Too much stock can look safe.

It can also quietly lock cash away, create waste, and give the business a false sense of security.

That is why working capital for small business is often shaped heavily by stock choices.

The practical questions are:

- what is moving quickly?

- what is slow-moving stock?

- what is sitting there mainly because nobody wants to make the awkward decision to clear it?

- what is seasonal and genuinely needed?

- what is just cash wearing a cardboard box?

There is a difference between smart stock and comforting clutter.

In my experience, businesses often call it “being prepared” right up until the moment they realise they have tied up too much money in things that are not moving.

When should you pay suppliers, and how do you protect both cash and trust?

Supplier timing is a working capital decision too.

Paying too quickly can tighten your own cash position unnecessarily.

Paying too slowly can damage trust, weaken reliability, and reduce flexibility when you need it most.

So this is not really about clever delay tactics. It is about balance.

A good leader asks:

- what terms make sense?

- what relationships matter most?

- where is flexibility possible?

- where would pushing too hard create more risk than benefit?

This is where real-world strategy matters more than textbook advice. A strained supplier relationship at the wrong time can cost far more than a few extra days of cash breathing room.

How much working capital does a business actually need?

A business needs enough working capital to operate steadily, absorb normal timing gaps, and avoid being knocked over by ordinary pressure.

That is the practical answer.

The more technical answer is: it depends on the business model, operating cycle, customer payment behaviour, stock needs, and short-term obligations.

Why does the answer depend on your business model?

Because not all businesses turn activity into cash at the same speed.

A service business with low stock and quick payment may need less working capital than:

- a retailer holding seasonal stock

- a manufacturer buying materials in advance

- a business growing quickly while customers pay late

- a firm with long project cycles and delayed billing

This is one reason generic advice only goes so far. Context changes the right answer.

Why is “more” not always “better”?

Because more working capital can sometimes mean trapped cash.

It may mean:

- excess stock

- weak collections

- too much idle cash

- inefficient use of resources

- decisions being delayed because the business feels artificially comfortable

This connects closely to how I think about decisions more broadly in the KrisLai Decision Framework™. More data is not always better data. More stock is not always safer stock. More working capital is not always healthier working capital.

Better decisions come from understanding behaviour, signals, environment, and consequences.

How do smart leaders make better working capital decisions when the future is unclear?

Smart leaders make better working capital decisions by using scenarios, watching behaviour, and acting before pressure becomes obvious.

That matters because the future is rarely tidy.

Costs move.

Demand shifts.

Customers delay.

Suppliers change terms.

People overestimate how quickly the good news will arrive.

Why should you use scenarios instead of one perfect forecast?

Because one neat forecast often creates false confidence.

I would rather see:

- a base case

- a pressure case

- and a best case

That gives you a better sense of range, not just one polished assumption pretending to be reality.

This is one reason I link strategy and uncertainty so closely on KrisLai. If you have not read it yet, this connects naturally to scenario planning and dynamic strategy.

Which behavioural traps lead to weak cash decisions?

In my experience, the big traps are usually human before they are mathematical.

Common ones include:

- overconfidence

- assuming customers will pay on time because they said they would

- chasing growth too hard

- ignoring early warning signs

- hoping timing problems will sort themselves out

- mistaking movement for control

- waiting too long because nobody wants to be the gloomy one in the meeting

This is where behavioural insight applied to business really matters. If you want to go deeper on that angle, it links naturally to behavioural economics in business and the wider question of how people really make decisions under pressure.

What does good judgement look like in day-to-day execution?

Good judgement looks boring in the best possible way.

It looks like:

- clear ownership

- regular review

- a simple dashboard

- honest conversations about pressure

- faster follow-up on warning signs

- fewer delayed decisions

- fewer comforting stories that keep the business sleepy

Good judgement does not need fireworks. It needs consistency.

How are AI and real-time data changing working capital decisions?

AI and real-time data are helping leaders see working capital patterns faster, but they do not remove the need for judgement.

That is the key point.

AI can help with:

- anomaly spotting

- payer-pattern detection

- invoice matching

- forecasting support

- inventory planning

- identifying drift earlier

That can be genuinely useful.

But leadership still matters because someone has to decide:

- which signals matter

- what trade-offs to accept

- when to push

- when to hold

- and what the likely consequences will be

Where can AI help most in day-to-day working capital management?

Usually in the routine, repetitive, pattern-heavy parts:

- spotting late-payer patterns earlier

- identifying stock that is moving too slowly

- matching invoice data more quickly

- helping teams update working capital views faster

That is support, not replacement.

Why does real-time or near-real-time information matter more than monthly reporting?

Because monthly reporting often tells you what has already happened.

Real-time or near-real-time information helps you see what is starting to happen.

That is a very different thing.

This also links to my work on AI and changing search behaviour. Leaders now search differently too. They ask more direct questions, expect faster answers, and often need practical judgement, not long theory. That makes clarity even more important.

What this looks like in real business

In a service business, the pressure often starts with slower-paying clients. Revenue may still look decent, but receivables creep out, payroll stays fixed, and the business starts carrying the load.

In a stock-heavy business, the problem may be too much money sitting in inventory that looks reassuring but is not moving. The warehouse feels full. The cash position feels less so.

In a growing business, sales may be rising while working capital gets tighter because growth itself is increasing strain. This catches people out more often than it should. Growth can look exciting right up until it starts strangling the cash position.

A business does not need to be in crisis for working capital to become a problem. More often, pressure builds through slower payments, excess stock, strained supplier timing, or growth that is moving faster than cash can support.

Where this goes wrong

Working capital goes wrong when leaders treat it as a formula to calculate rather than a system to watch.

That usually shows up in a few familiar ways:

- focusing on profit while ignoring liquidity

- leaving receivables to drift

- carrying too much stock

- leaning too hard on short-term borrowing

- paying suppliers badly and damaging trust

- assuming the business has more room than it really does

- reacting late because the warning signs looked small

What I have seen is that these problems rarely arrive one at a time. They tend to travel in groups.

A late-paying customer here.

A little more stock there.

A supplier call nobody wants to return.

A bit more pressure on the overdraft.

And suddenly the business is “surprised” by something it has actually been signalling for months.

- Leaders wait for a cash crisis instead of reading early signals

- The business tracks profit but not payment timing

- Stock looks safe but quietly traps cash

- Supplier timing is treated as a tactic rather than a relationship decision

- Working capital is reviewed too late, too rarely, or too mechanically

What you should actually do

If you want to manage working capital better, I would keep it practical.

- Review receivables honestly

Who pays late, how often, and what is drifting? - Look at stock without romance

What is genuinely needed, and what is just sitting there looking important? - Review supplier timing properly

Where can terms help, and where would pressure damage trust? - Track one or two early-warning measures

Not just the formula. Watch the pattern. - Use simple scenarios

Base case, pressure case, best case. - Review it monthly as a leadership issue

Not only as a finance task.

This connects closely to how I think about decisions more broadly in the KrisLai Decision Framework™. The point is not to become obsessed with one metric. The point is to notice the signals early enough to act well.

Smart leaders do not wait for working capital to become a cash emergency. They watch the smaller changes first, ask what those signals mean, and act while they still have room to choose well.

Conclusion and Final Thoughts

Working capital is not just a definition, a formula, or a line in a finance glossary.

It is one of the clearest ways to see whether the business is steady, stretched, or drifting into pressure.

That is why smart leaders watch it early.

They do not wait until cash gets tight and everyone suddenly becomes very interested in the bank balance. They look at the quieter signals first: how fast customers pay, how much stock is tied up, how suppliers are being managed, and whether the business is building pressure faster than it realises.

In my experience, strong working capital control is a leadership skill.

It is part finance, part discipline, part judgement, and part willingness to act before the problem becomes obvious.

Working capital is not just a finance measure. It is an early warning system for cash pressure, operating strain, and weak timing decisions. Smart leaders watch it before cash gets tight, act on small signals early, and use it to protect resilience when the future is uncertain.

PS. If you want to strengthen this side of the business further, the best next step is to connect working capital with your wider decision tools. Read next: Cash Flow Forecasting for Better Decisions Under Uncertainty, Financial Dashboards That Help Leaders Make Better Decisions, 5 Financial Ratios Every Business Leader Should Understand, How AI Is Changing Search Behaviour, Behavioural Economics in Business, Scenario Planning, and Psychological Safety at Work.

If you want to strengthen how you make decisions under pressure, I’ve put together a free guide to The KrisLai Decision Framework™ — a practical way to spot signals early and act more clearly.”

Free Guide: Better Business Decisions Under Pressure

Financial pressure rarely begins with one dramatic event. It usually starts with small signals that are easy to miss.

Enter your email below and I’ll send you the free KrisLai Decision Framework™ guide, a practical model for understanding behaviour, signals, environment, and consequences before problems become more expensive.

It is designed to help leaders think more clearly and act earlier when timing, pressure, and uncertainty begin to build.

Frequently Asked Questions

What is working capital?

Working capital is the difference between a business’s current assets and current liabilities. It helps show whether the business has enough short-term resources to meet its short-term obligations.

What is the working capital formula?

The working capital formula is current assets minus current liabilities. It is used to assess short-term liquidity and day-to-day financial stability.

Why is working capital important?

Working capital is important because it helps a business keep operating smoothly, pay bills on time, manage pressure, and avoid short-term cash strain.

What does negative working capital mean?

Negative working capital can mean that short-term liabilities are higher than short-term assets. In some cases that signals pressure or risk, although the meaning depends on the business model and operating cycle.

How can a business improve working capital?

A business can improve working capital by collecting receivables faster, managing stock more tightly, reviewing supplier payment timing, improving forecasting, and acting earlier when pressure starts to build.

If you enjoy exploring the ideas behind better business decisions, you may find the Business Thinking Hub useful.

About the author

Kris Lai is a business operator and managing director with experience in land and building surveying, facilities management, logistics, and service delivery.

Earlier in his career, he worked as a Search Engine Evaluator (via Lionbridge, supporting Google), where he assessed search result relevance, user intent, and content quality using structured evaluation frameworks. This experience gives him a rare, practical understanding of how search systems interpret signals and make ranking decisions.

In parallel, whilst working with a charity organisation, he has delivered 1000’s of structured presentations in English, Finnish, and Chinese to audiences ranging from small groups to more than 600 people, and has spent decades mentoring and developing others. This experience informs his approach to clarity, communication, and decision-making under pressure.

He writes about AI, search behaviour, business strategy, and decision-making from a practical, real-world perspective.

👉 Explore ideas connected to better business decisions:

- How AI Is Changing Search Behaviour (And What Businesses Must Do Now)

- Decision-Making Framework Examples: The KrisLai Method in Action

- The KrisLai Decision Framework: A Better Way to Make Business Decisions

- Micro vs Macro Marketing: When to Target Broad Audiences vs Niche Customers

- Customer Intent Marketing: How to Turn Buying Signals Into Sales